A few weeks ago, Canadian Prime Minister Mark Carney announced Canada’s first ever national sovereign wealth fund: The Canada Strong Fund.

We posted about it on our Instagram, and comments came flooding in. Some of them were genuinely sharp. Others were, well, the internet being the internet.

“Sovereign debt fund!” “Government-backed Ponzi scheme!” “Canada is cooked!”

But the critics aren’t entirely wrong, and neither are the people defending it. What Carney proposed is an innovative, unique, complicated idea, executed in an unusual way, by someone who probably knows more about fund management than any living Prime Minister anywhere.

So when a government announces a new sovereign wealth fund, I pay attention.

In this issue, I'll break down how the fund actually works, make the case for both sides, and highlight what to watch in the months ahead.

Let’s go. 👇

Unicorns aren't IPO’ing like they used to

But we found a way to invest in them.

Back in 1980, the median age of a company at IPO was 6 years old. By 2025, that figure had nearly doubled according to research from the University of Florida.

With companies staying private twice as long as they did decades ago, it’s become more difficult for investors to gain exposure to them. Which is a shame, because more and more of them have grown to be unicorns.

So what do retail investors do? We found a company that can help you gain exposure to unicorns…

Think of it as a robo-advisor for the secondary market — a $10k minimum gets you exposure to a diversified basket of private companies that until recently lived behind a wall of navigating complex private transactions and significant investment minimums.

How it works

Pick a strategy: You pick a pre-built automated strategy or choose specific companies.

Heron builds your exposure: Heron uses their institutional access to purchase private company shares as they become available, building your exposure over time.

Heron manages it for you: Automated strategies are rebalanced for you, adding the latest top companies as they become available.

Disclaimer: Investing in private, pre-IPO companies involves significant risk and is not suitable for all investors. These investments are generally illiquid, may be difficult to value, may be subject to transfer restrictions, and may result in the loss of some or all of your investment. Any information provided is for informational purposes only and should not be viewed as investment, legal, or tax advice or as a recommendation to buy or sell any security. Past performance, estimated valuations, company growth, or secondary market pricing are not indicative of future results. Pre-IPO companies are privately owned and not all private companies will experience an IPO or other liquidity event.

What is this fund, actually?

The Canada Strong Fund is a government-owned investment vehicle designed to co-invest alongside private capital in national infrastructure projects.

Think ports, mines, energy, agriculture, etc. The kind of large-scale stuff that private investors avoid because the timelines are too long.

A render of LNG Canada Phase 2 Project in Kitimat, BC. Canada sits on enormous natural resource wealth but has long lacked the infrastructure to develop and export it at scale. This project would 2x the facility's output and make it the second largest LNG export terminal in the world. The Canada Strong Fund is designed to help change that.

As for how it came to be: Carney simply announced it on April 27th. It wasn’t put to a vote. Rather, the funding was embedded into the budget; which is common in Parliamentary systems like Canada's.

The legislation to establish the fund’s structure is still being worked through. The money has been committed, but the plumbing is still being built.

The government is initially coughing up $25 billion over three years. It will be run as a "Crown Corporation" — a government-owned entity with and independent CEO and board, designed to operate at arm’s length from day-to-day political interference, while still being accountable to Parliament. (Think Canadian Broadcasting Corporation, or Canada Post.)

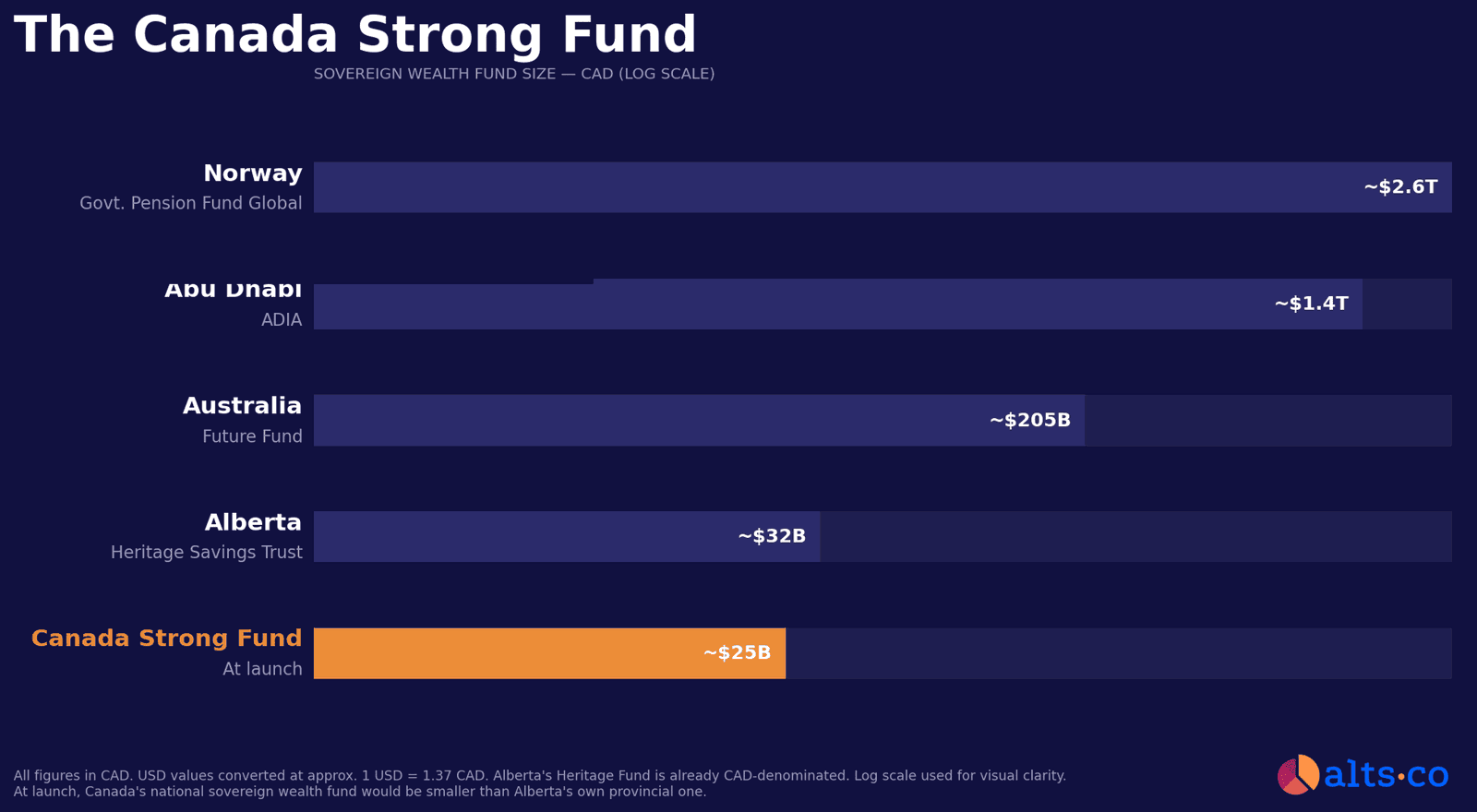

To put the scale in context, the Canada Strong Fund launches with $25 billion CAD. Norway's fund sits at around $2.6 trillion. Abu Dhabi's is close to $1.4 trillion. Australia's Future Fund — a more comparable Western nation — is around $205 billion. Even Alberta's own Heritage Savings Trust Fund, a provincial fund built from oil royalties over five decades, currently sits at around $32 billion.

At launch, Canada's national sovereign wealth fund would be smaller than Alberta's provincial one. But it's still a good start.

What's interesting about this fund is that individual Canadians will be able to invest directly.

Yes, Norway, Singapore, and Abu Dhabi all have sovereign wealth funds. But none of them let ordinary citizens buy in directly! Canada is proposing something different: you put money in, you earn a return.

On paper, it sounds reasonable. The catch (and it’s a significant one) is how the government is funding its own $25 billion contribution.

The problem with the name

Every serious sovereign wealth fund in the world was built from surplus.

Norway’s fund (the world's largest, now worth $1.9 trillion) was seeded with excess revenue from North Sea oil. Abu Dhabi’s was built on petrodollars. Even Alberta’s was funded from oil royalties the government had already collected.

But in Canada, the federal government is running a deficit. There is no surplus. So the $25 billion is being borrowed.

Specifically, Canada will raise the money the same way it finances any spending beyond its tax revenues — by issuing government bonds which get scooped up by institutions, foreign governments, pension funds, and asset managers around the world.

Critics on our Instagram called it a “sovereign debt fund.” That’s a little glib. But it’s not entirely wrong.

As of the announcement, Canada’s 10-year government bond yield sat at around 3.5%. That’s the cost of capital. So before this fund generates a single dollar of real national wealth, it needs to clear a return hurdle of 3.5%.

Carney’s finance minister pointed to Canada’s relatively strong credit rating and its ability to borrow at favorable rates internationally. Which is true. But as the Globe and Mail noted, it means the math is tighter than the announcement made it sound.

The bull case

So why might this actually work?

Let's start with the problem it’s trying to solve. Infrastructure is incredibly important to societies, yet private investors (even alternative investors) often stay away from it.

Like many countries, Canada has a serious infrastructure gap, which private capital hasn’t filled on its own. A government vehicle designed to co-invest alongside private capital is a reasonable idea!

The idea of citizens co-investing in national infrastructure isn't new. Venice financed its ports, Arsenal, and trade network through the prestiti — a system where citizens lent money to the Republic and received interest in return. It was one of the earliest government bond markets in history. Canada's retail component is the same idea: you invest in the country's buildout, you share in the return. (Apologies for all the Venice references lately. I've been reading Venice: A New History by Thomas Madden!)

Then there’s Carney himself. You can debate the policy, but it’s hard to argue with the guy's resume.

Former Governor of the Bank of Canada. Former Governor of the Bank of England. The man literally helped steer the global financial system through the 2008 crisis. If anyone understands how sovereign capital should be deployed, it’s probably him.

Now let’s talk returns, because the government hasn’t published a specific target, just the phrase “market-rate returns.”

So what does that actually mean in practice?

Well, the The average 10-year return across sovereign wealth funds globally is around 6.3%. Norway’s fund has averaged 6.6% annually over its lifetime. A classic 60/40 portfolio of stocks and bonds has returned roughly 7.9% over the same period. Those are your reference points.

Our Altea SPV returns have been much better. Ahem.

Anyways, against a borrowing cost of 3.5%, here’s how the scenarios shake out.

If the fund performs like an average global SWF, you’re looking at a net spread of around 2.8% before operating costs. Not spectacular, but a real return on national capital.

If it performs more like Norway, the net spread above borrowing costs is around 3.1%. That doesn't sound like much — but applied to $25 billion over 30 years, it compounds to roughly $36 billion in real wealth generated above the cost of capital. That's the difference between a fund that merely justifies its existence and one that genuinely transforms Canada's fiscal position.

If the fund performs, ordinary Canadians get a bond-like instrument tied to national economic growth.

The honest bull case isn’t that this fund will definitely generate great returns. It’s that Canada has a real infrastructure problem, a credible architect, and a reasonable structural template — and that if it’s run with genuine independence, there’s a path to it becoming something real over time.

The bear case

Here’s the scenario that makes bears worried.

Ireland runs a domestically focused sovereign fund. It's similar in structure to what Canada is proposing. Over the past decade it has returned around 3.4% annualized. That's less than Canada’s borrowing costs of 3.5%. If Canada's fund gets 3.4% returns, it's indeed cooked.

Then there’s Canada’s own track record. In 2017, Trudeau government launched the Canada Infrastructure Bank with a $35 billion mandate, and near-identical rhetoric about private capital & national infrastructure.

However, nearly a decade later, Canada’s own Parliamentary Budget Office stated it would disburse less than half that (around $14.9 billion) by its 2028 deadline. Worse, roughly two-thirds of its co-investments came from public partners rather than private ones, the opposite of what it was designed to achieve!

Finally, there’s the durability question. Norway’s fund works partly because it was architected to be bipartisan. It has survived decades of government changes without being dismantled. But Canada’s Conservative opposition has already called Canada Strong Fund a “sovereign debt fund” and shown no sign they’d preserve it.

The structure of the fund is supposed to guard against this. (Independent board, arm’s-length Crown corporation design, etc). But note that the founding legislation hasn’t actually been written yet, so key questions remain unanswered:

How clearly is political interference prohibited?

How is the CEO appointed and removed

What stops a future government from redirecting the fund toward projects that are politically convenient rather than commercially sound?

“Investing in projects that can change on political whim, seems shaky...no?” — @stef_mart, Instagram

Closing thoughts

I'm not a Canadian citizen or resident, so my opinion doesn't mean much: But I generally agree with this comment:

Carney served as chair of Brookfield Asset Management before becoming PM, holding stock options and future performance pay worth tens of millions. Critics argue this creates a conflict of interest, while Carney maintains he has exceeded ethics requirements through a blind trust and conflict of interest screen. Regardless, compared to Trump's corruption south of the border, something like this barely qualifies as a footnote.

The most liked comment on our Instagram post wasn’t from a critic or a cheerleader:

“Norway and Singapore are great examples of why this is a good idea, but those are countries where the government enjoys high trust. It has to be well run and prestigious enough to attract talent to manage it.” — @still_very_dodgy (173 likes), Instagram

This is a critical point right here.

The Canada Strong Fund is not a bad idea in principle. The infrastructure gap is real. The co-investment model is sound. The retail component is interesting. And Carney is definitely well-positioned and well qualified to pull this off.

But the way this fund is architected will be critical, because none of that matters if the fund becomes a political instrument or gets dismantled the moment the government changes.

No CEO has been named. The founding legislation that will define how much independence the fund has hasn’t been written. The retail investment product is still being designed. The government has said all of this will be resolved “in the coming months,” but no specific timeline has been given.

And a constitution-protected wealth fund that compounds for fifty years is a completely different animal from one that gets restructured every election cycle.

Right now, nobody knows which one this will be!

So in the meantime, this should be watched closely:

When they name a CEO, look at whether it’s a genuine capital markets appointment or a political one.

When the legislation drops, read the governance provisions carefully. They’ll tell you more about what this fund is really meant to do than any press release will.

And watch whether the Conservative opposition shifts its position as the fund takes shape, because without some degree of political durability, the compounding that makes sovereign wealth funds genuinely powerful simply won’t happen.

The fund was announced four weeks ago. The next few months will tell us whether Canada is building something real and lasting. 🇨🇦