Japan resisted change for 30 years. Then Covid did what decades of pressure couldn't. With the old guard gone and the Nikkei at all-time highs, capital is moving fast.

In preparation for the trip, I'm exploring all sorts of Japanese investment themes. Things I'm curious about, stories we're hearing, and corners of the economy that seem under-appreciated.

In Part 1 back in March, we covered the tourism supercycle, the culture of craftsmanship & longevity, and hyper-niche specialty manufacturing. Prior to that we explored investing in Japanese whisky and even Bonsai.

Today in Part 2, we'll explore the huge generational shift that's remaking corporate Japan, and why the country has become the world's second-largest private equity engagement market.

This week, I attended the Jefferies Japan Thematic Summit in Melbourne — an exclusive, invitation-only investment event connecting Japan investors, operators, and analysts with prominent Japanese companies.

This event brought together leading Japanese companies, institutional investors and market experts to discuss Japan’s structural transformation and growing importance to global investors.

This issue connects two threads through one line: the generational change remaking corporate Japan, and the private equity opportunity that exists because of it.

Let’s go 👇

1031 exchange: The most underused tax tool in real estate

Most investors contact Tom Bottenberg after they've already listed the property.

By then, the clock is already ticking, and in a 1031 exchange, timing is everything.

Here's what lots of real estate investors don't know: Section 1031 of the tax code lets you sell an investment property, roll the proceeds into a new one, and defer your some of not all your capital gains tax entirely. Not avoid, defer. Indefinitely, if done right.

Tom from Institutional 1031 has helped thousands of investors use this tool to compound their wealth over time. The ones who benefit most are the ones who planned before they decided to sell.

Once a 1031 starts, the IRS gives you 45 days to identify a replacement property and 180 days to close. Miss that window, and you're writing a check you didn't have to write.

Want help doing a 1031 Exchange?

If you own investment real estate and have even a passing thought of selling in the next year or two, now is the time to talk.

Tom personally welcomes these conversations. Whether you have a deal in motion or are just starting to think it through. No pressure, no pitch. Just a straightforward discussion about whether a 1031 makes sense for your situation.

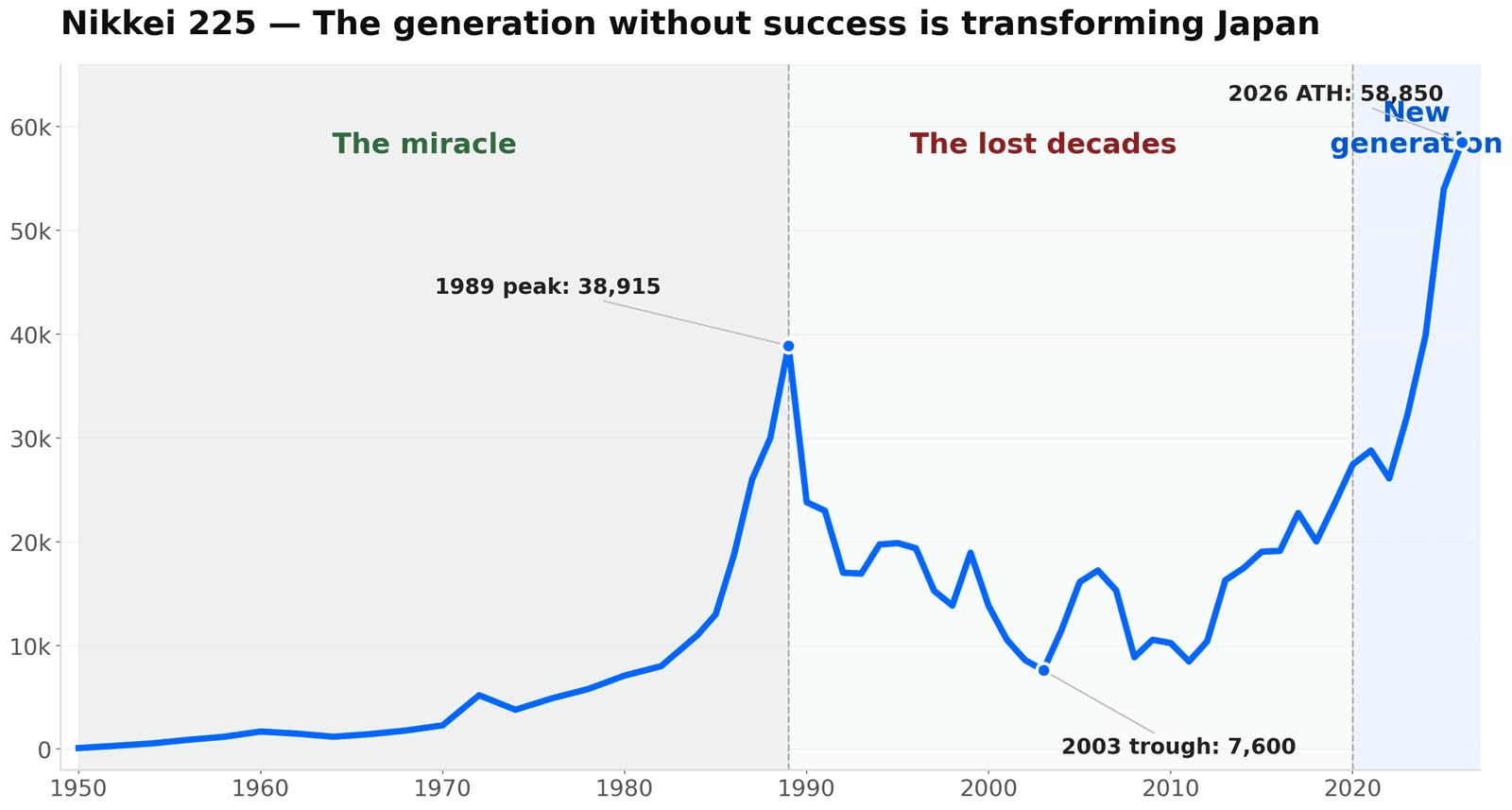

Japan’s post-war economic miracle is one of the great stories of the 20th century.

The country went from rubble to the world’s second-largest economy in just 25 years. The Nikkei was climbing for decades, terrifying Americans as corporate Japan started winning at everything: electronics, steel, semiconductors, cameras, and especially cars:

Aside from China, no country has had a larger effect on global auto markets than Japan. By 1980, Japanese cars claimed 30% of the US market

The leadership class that oversaw all this became, understandably, deeply confident in themselves and their methods.

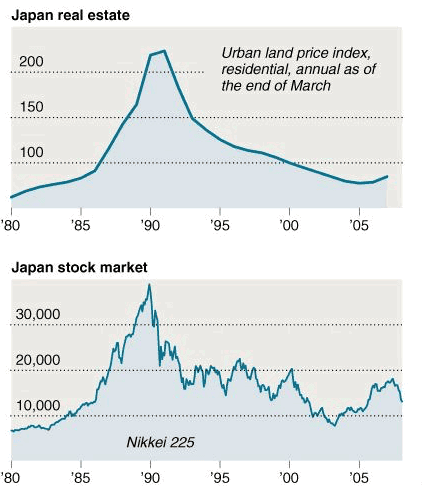

Then 1989 happened. The bubble burst, and the world moved on.

One of the largest asset price bubbles in modern history. Japanese stocks and urban land values had tripled in just four years. At its peak, the Imperial Palace grounds in Tokyo were estimated to be worth more than all the real estate in California! When it burst, it took three decades to recover. Sources: Standard & Poor's; Japan Real Estate Institute

But here's the part that people miss: Japan’s leadership class didn’t.

See, Japan's leaders had succeeded so spectacularly for so long, that they simply couldn’t process why change was needed. When foreign investors and outside voices told Japan it needed to reform, the response was roughly: "We built a miracle. Why should we listen to you?"

So from 1989 until COVID, they basically didn’t.

COVID achieved what boardrooms couldn't

Seniority in Japan is like a social operating system. Promotions aren't really about merit or competence. Deference flows upward, always. The older you are, the more your word carries.

Nenkō joretsu is the Japanese system of promoting an employee purely in order of their proximity to retirement.

For years any generation handoff occurred purely on paper. New CEOs took the chair while the old guard stayed on as “senior advisors,” occupying the room next door, their informal influence still shaping every decision.

Powerful elderly senior managers proved unwilling or unable to shift. Any generational change was nominal. The old guard was still running things.

Then COVID happened. The senior people left the office in 2020. And they never came back.

The result is a long-overdue changing of the guard. For the first time since WW2, a real generational disconnection has occurred in Japan.

It took a global pandemic to physically remove power structures that had been blocking change for three decades, and the office never reopened for them.

Japanese stocks have been on a tear since then. In fact, just yesterday indices hit another all-time high. This time, momentum feels structural rather than cyclical.

The Nikkei 225 tells the whole story. A 40-year miracle, followed by three decades of stagnation. Now, freed from the past, a new generation has taken a seat at the decision-making table as the Nikkei reaches all-time highs.

Today, the new generation is now actually running things. And this generation, which entered the workforce after the peak and has only ever seen Japan underperform, is fundamentally different. They listen to outside voices. They take action. They’re willing to learn from others.

And for the first time in a long time, the political establishment is moving in the same direction.

Enter Sanaenomics

You may have heard the term "Abenomics." It was Japan’s last big macro experiment under Prime Minister Shinzo Abe: monetary easing (lower interest rates), fiscal stimulus, and structural reform, all in the name of stimulating demand.

Abenomics succeeded in ending deflation (hooray!) and generated five million jobs. But it raised the consumption tax twice while trying to stimulate demand (yes, really), and never achieved a consistent 2% inflation target. Something was always working against itself.

Now, there's a new sheriff in town: Prime Minister Sanae Takaichi, Japan's first female PM.

When she took office in October 2025, Takaichi announced a new framework (informally called "Sanaenomics") which centers on supply-side investment rather than demand stimulus.

Essentially, Takaichi wants to boost the capacity of the Japanese economy, not just spend to create activity.

Japan's policy focus has shifted from aggregate demand to supply-side investment. Semiconductors, data centers, energy, and strategic manufacturing. The timing is almost lucky: a government willing to spend aggressively on capacity at the exact moment the world is short on supply.

Prime Minister Takaichi arrived with a supermajority in the lower house, something never seen before in postwar Japan, and a clarity of agenda that has surprised even close observers of Japanese politics.

She even reportedly wrote a two-page memo to each of her ministers, with specific orders and clear direction, then published them. Anyone can read what she told the Minister of Finance, the Minister of Economy, each one individually. That level of transparency is new.

The execution is already visible. For example, Taiwanese chipmaker TSMC wanted to build outside Taiwan for security reasons. They chose sites simultaneously: Kumamoto, Japan, and Arizona.

Arizona's construction started in 2021, Kumamoto's in 2022. Despite starting one year later, Kumanoto finished production a year before Arizona.

The difference is that Japan’s government streamlined every approval, resolved every complication, and moved at a speed that would have seemed impossible a decade ago.

The Hokkaido Technology Corridor is Sanaenomics in practice. It's centered on Rapidus, Japan’s government-backed 2-nanometer chip facility near Sapporo, now drawing memory companies, fiber producers, and precision manufacturers into a purpose-built semiconductor cluster.

New Japan: Open doors, open ears

My favorite session from this week's Japan Thematic Summit was from James Halse.

You may recognize James from the roster of our Japan trip. In 2024, James co-founded Senjin Capital alongside Tsubasa "Toby" Umezaki. Senjin is one of the only funds in the region built specifically around using shareholder activism to unlock value in Japanese small and mid-cap companies.

In my opinion, his speech captured Japan's zeitgeist shift better than any chart possibly could.

Here’s how James tells it:

"A decade ago, you'd speak to a company that had 30 - 50% of its market cap in cash, and you'd spend 90% of the call talking about the business. You get to the last five minutes and say, 'So you've got half your market cap in cash. What are you planning to do with that?' And the company would say, 'Oh, well, we need that cash to fund our CapEx plans and our R&D.' And you'd look at their presentation and say, hold on — all of that is funded by your projections for operating cash flow. So your cash is actually just...building up? They'd say, 'Oh, well, yes, we'd like to do some M&A. 'Great,' I'd say. 'Are you planning on actually doing any M&A? Are you looking at targets? Do have a team?' 'No, we're not planning on doing any.'

'Are you thinking about it?

'No, we would like to think about doing some.'

'So you're thinking about doing it?'

'Oh, no. We'd like to think about doing some.'

And round and round we go. As James put it, this is a very, very Japanese answer.

Fast forward to about five years ago. Same call, same question. The conversations had evolved:

'Oh, yes, yes. We've started doing a small buyback. We've increased our dividend payout ratio to 50%. And we're thinking about increasing the buyback. We've got some cross-shareholders who want to sell, so we'll do some opportunistic buybacks as well.'

And finally, fast-forward to today. James recently had a call with the very first company Senjin invested in. The team in Japan got halfway through the call and said:

'So James, you're an engagement fund. We know we have far too much cash. What do you think we should do with it?'

Boy, how times have changed!

That attitude is new. That’s Japan now.

"Companies know they need to do things. To be clear, they don't really want to give up their cash or operate more efficiently, they're quite happy and comfortable and cozy. But they kind of know they're supposed to." — James Halse

James is far from the only player who's been on top of this shift.

KKR, Carlisle, and Bain have been raising record funds for Japan, and are now basically openly competing with each other for public assets, unusual behavior for an industry that typically moves "behind the scenes."

The secret is out. Private equity deals in Japan reached record highs in 2025.

And the conditions that created this didn’t happen by accident.

What caused Japan's PE gold rush?

Regulatory + shareholder pressure

The Tokyo Stock Exchange (TSE) lists nearly twice as many companies as the NYSE. The truth is, many of them probably shouldn't be there.

In 2023, the TSE started telling companies that if their return on equity is below their cost of capital, they need a plan to fix it.

The Tokyo Stock Exchange publicly shamed companies trading below book value and made clear that management needed a credible plan to address it. This was not a suggestion. Boards took notice. You don’t ignore the exchange that lists you.

Why did the TSE do this?

Simple. When rates are near zero (like they were for decades), holding cash costs you nothing. Your company sits on a pile of yen, earns nothing on it, but loses nothing either. There's no pressure to do anything with it.

But now that the risk-free rate is rising, the calculation has changed. Shareholders ask: "Why is our money sitting in a corporate bank account earning 0.5% when we could deploy it elsewhere for a better return?"

The opportunity cost of holding cash becomes real and visible. Suddenly companies that were coasting have to justify their cash hoards or face activist pressure to return it.

Japanese law is wildly favorable to outside investors

In Japan, a buyer can reach squeeze-out threshold and take full control of a company at 66%, the lowest of any developed market. (Australia, the UK, and Singapore all require 90% or above.)

There are also no creep provisions (a tactic to deter hostile takeovers). This means you can acquire 30% of a company overnight without triggering a mandatory bid for the rest.

Remember, the government is well aware of the oversupply of Japanese public companies. Just last week they began encouraging private companies weighing an IPO to consider a PE sale instead.

Private equity math in Japan works in a way it simply doesn’t elsewhere right now.

Boards are no longer an 'old boys club'

This all comes during a time when board composition is shifting.

Nearly all of Japan's top listed companies now have at least a third of their board seats occupied by outside directors (up from almost none a decade ago).

While it may seem counter-intuitive, foreign activists often have an easier time in Japan than domestic ones.

After all, the comfortable "consensus culture" which protected mediocre capital allocation for decades is harder to maintain when the room now contains people who didn’t come up through the same system.

Activism carries real social cost. In Japan, a foreign investor carries no such baggage. No ol' boys network to be expelled from. The activist community in Japan skews heavily international for exactly this reason.

James (middle) takes a "good cop, bad cop" approach. He starts constructively, engages management, presents a clear thesis, and give them every opportunity to act. Most of the time that’s enough. When it doesn't, he escalates. Often the most effective next move is simply patience, because there’s a ready buyer for almost every asset in Japan right now.

The presence of a credible activist on the register tends to focus minds.

Meanwhile, as activists like James work the public markets, PE firms work a private conversation. Their message to management is simple: "Look team, we can make all this shareholder pressure go away. Come with us. And take a meaningful equity stake in the upside."

INSIDE LOOK: The Toshiba Story 👀

When Toshiba was forced to sell its memory business to plug a financial hole, Bain Capital acquired it, and gave roughly 5% of the company to around 800 employees. Not just the board, but director-level people throughout the organization. When the stock ran after IPO, employees who had never earned more than the equivalent of $100,000 a year found themselves sitting on an average of around $5 million each! PE often gets a bad rap, but stories like this travel. It gets told at dinners and golf clubs and industry events. And it changes how Japanese management thinks about what a PE transaction can actually mean — for them personally, and for their employees.

⛩️ Want to come to Japan?

Early bird pricing ends tonight!

Our investor trip to Japan is happening October 18–22.

This is adventure capitalism at its finest.

Experience Japan like an insider, meet captivating people, and enjoy this once-in-a-lifetime travel adventure.

Everything covered except your flight: 4 nights of hotel, all meals, all drinks, in-country transport including the shinkansen up to Nagano, every activity, every speaker session.

Early Bird (ENDS TONIGHT): $3,499

Standard (June 1+ onwards): $3,999

Final Call (Sept 1+ onwards): $4,499

Bring a guest at any tier: +$2,999

This is the highest demand we've ever had for an investor trip. There are 5 spots left, and they absolutely will not last long.

$1,000 holds your spot. It's fully refundable up to 60 days before the trip.

If you're on the fence about joining, I suggest you put the deposit down now. The price goes up by $500 tomorrow.

Closing thoughts: Capital is coming home

For years, Japanese households parked their NISA (Japan’s tax-advantaged investment account, similar to an ISA or Roth IRA) allowances into S&P 500 ETFs and global equity funds that explicitly excluded Japan. Investing at home felt like a losing proposition (because for a long time it was.)

That has changed. The number of individual shareholders in Japan hit a record 83.6 million in 2024 — up 9 million YoY.

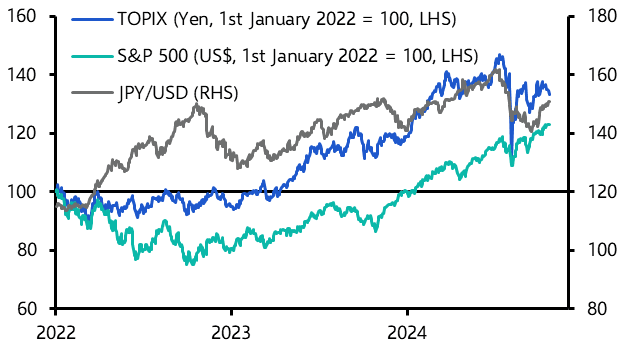

TOPIX, a major stock market index for the Tokyo Stock Exchange, has actually outperformed the S&P 500 by roughly 40% over the past five years. However, while this looks fantastic on paper, the massive depreciation of the Japanese Yen will significantly erode those gains if converted back to an investor's home currency.

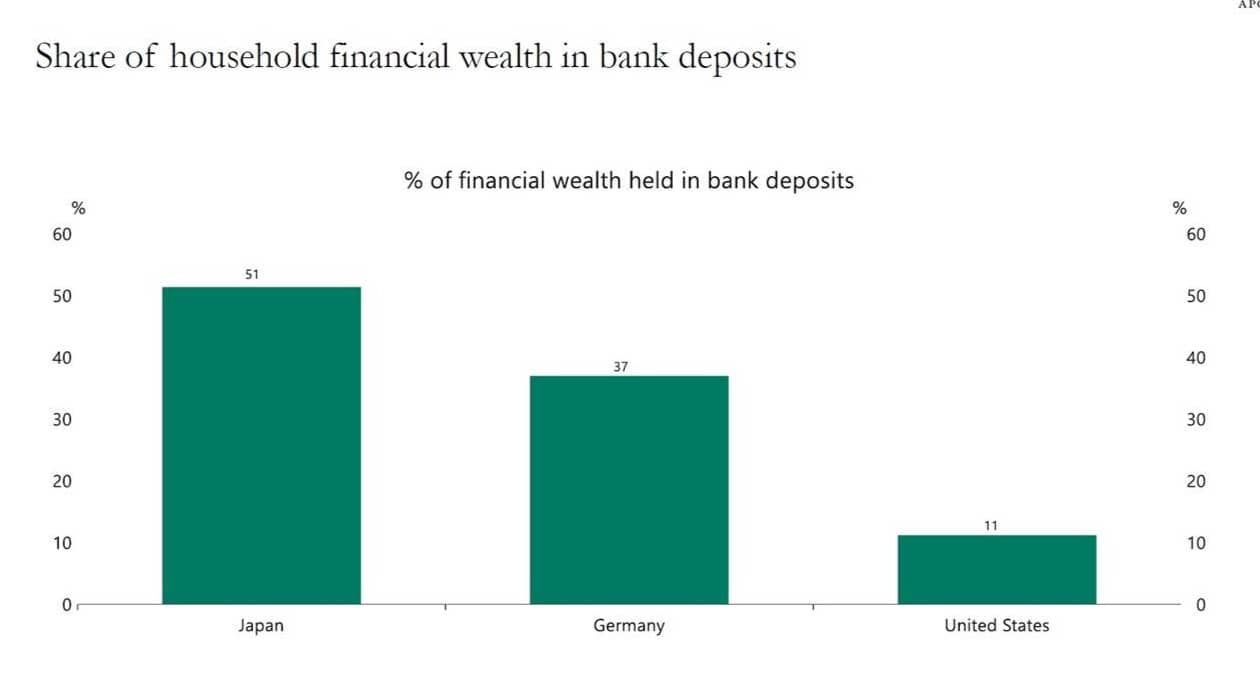

As we discussed in Altea a few months ago, an astonishing 51% of Japanese household financial wealth currently sits in bank deposits.

But as Japan "re-inflates" and interest rates go back up, holding cash means losing value! And lots of this cash should theoretically make its way into equities.

This has been the foundation for a bull case in Japanese equity markets for a long time. If you can shift even a small percentage of exposure to public markets, well, all that capital has to go somewhere, right?

Investors like James who figured out where are having the best decade of their careers. 🇯🇵

---

That's it for today.

I hope you enjoyed Part 2 in this series on investing in Japan. A big thanks to James Halse and Jefferies for a terrific event this week.

Part 3 will be on Japanese real estate.

In the meantime, our trip to Japan is happening October 18-22. Only five spots remain. They'll be gone soon. Secure your spot now.

Until next time, Stefan

Disclosures

This issue was written and edited by Stefan von Imhof

This issue was sponsored by Institutional 1031.

Alt Assets, Inc has no current holdings in any companies mentioned in this issue. We are planning on creating an SPV with Senjin Capital in late 2026.

Recent emails from Alts

Shop without the noise

Get our free newsletter of hand-picked sales you need to hear about from the web's best brands.

There was a problem subscribing this email address

Good stuff coming your way!

ProTeam

Your account is managed by your organization. Contact your administrator for access to Pro features.