For 90 years, Australia had a "cheat code" for property investors. Now it's being taken away, and the implications are big.

Welcome to the Alts Sunday Edition 👋

This week, on the heels of our second real estate SPV, we're continuing our international real estate kick, with a look at a very significant development happening down under.

There’s a running joke here in Australia that every conversation, no matter where it starts, eventually turns to real estate.

I've experienced this firsthand, and can confirm it's absolutely true. You'll start out discussing the weather or sports or AI, and before you know it everyone's talking property.

Dinner parties. Work lunches. Family barbecues. Someone always knows someone who made a killing selling in Double Bay. Someone’s cousin bought in 2019 and their place has already doubled. It's comical.

Australia is arguably the single most property-obsessed nation on earth. And for good reason — it's been a borderline unstoppable market for decades.

Celebrating BBQ, beers, and another year of double-digit appreciation!

But now things are about to change. The "unfair" tax law that turned ordinary Australians into leveraged property investors is coming to an end, and the implications go far beyond the shores.

The law is called negative gearing, and in this issue I'll explain exactly what it is, why it's so controversial, and what happens now that the government is about to unwind it.

For alternative investors outside Australia, this matters. When a $1.4 trillion property market becomes less desirable, capital moves. The only question is where.

Let’s go 👇

Get alts in your retirement fund

Get more from your alternative investments with a Self-Directed IRA.

If you're reading Alts, you already know the power of investing in alternative assets. But if you're not using a Self-Directed IRA, you might be missing out.

Our friends at IRA Financial let you put your retirement dollars to work and give you the freedom to invest in what you believe in.

With a Self-Directed IRA, you get:

Access to additional capital by transferring or rolling over existing retirement accounts

Tax-deferred or tax-free growth

Capital gains shelter

Estate planning benefits

With IRA Financial you get the full tax advantages of a retirement account. That means your alternatives grow tax-deferred (or tax-free), so you keep more of your gains.

What do they offer?

Self-Directed IRA (SDIRA). Full alternative access, same tax advantages as a traditional IRA

Checkbook IRA. Write checks directly from your IRA LLC, no custodian sign-off on every trade

Solo 401(k). Built for self-employed investors and business owners

Self-Directed HSA. Even your health savings account can invest in alternatives

What sets IRA Financial apart?

Flat fee. No asset-based or per-investment charges

Tax and compliance support. In-house. You don't need to navigate the rules alone.

History. 27,000+ active accounts, $7B+ in assets invested 4.8 stars on Trustpilot. A+ BBB rating.

Real-time. Powered by Interactive Brokers, you can invest in stocks, mutual funds and other traditional assets in real-time, in the same account as your alternative assets.

As an Alts subscriber, you get $100 off your first year fees of any account. Express interest to get your code.

Self-directed retirement accounts involve risk. IRA Financial does not provide investment, legal, or tax advice. Consult a qualified financial or tax advisor before investing.

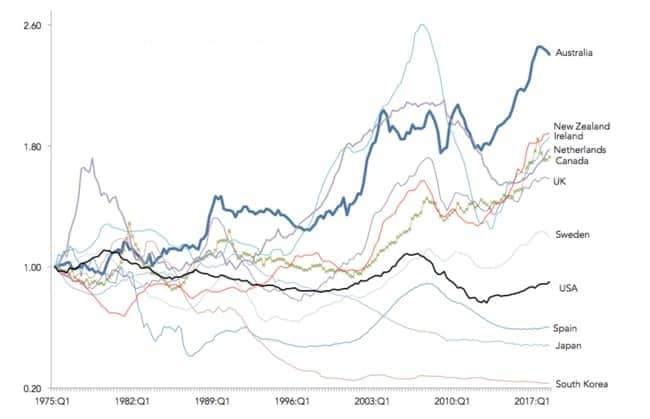

How Australia became the world's most property-obsessed nation

The first thing you need to know is Australian real estate has been nearly invincible for decades.

Aussie home prices have risen an average of 6.4% per year for the past thirty years. Sydney, Brisbane, and Perth have each delivered more than 7% annually over forty years. The national median has risen 540% since 1983.

But what really sets Australian real estate apart is resilience. During the early 90s recession, prices rose in most markets. And while the world was suffering the GFC, here in Australia the median price actually increased in nearly every capital city the following year.

During the 2008 crash, US real estate fell 30% peak to trough, while the UK, Canada, and other countries had serious corrections. But Australia sailed through the crisis with nary a scratch. Few Anglosphere countries have managed this level of resilience.

The reasons are structural: relentless high-skilled immigration into a handful of coastal cities, chronic undersupply, and a tax system explicitly designed to reward property investment. We'll get to that in a minute.

This week I sat down with Altea community member Esha Frykberg, a Partner & Finance Broker at Melbourne-based Market Street Finance. It only took a few beers for Esha to admit what every Australian already knows deep-down:

“It’s ridiculous that you can make more money from property than from a job. It’s insane.”

He’s not wrong. When home values are rising at 10.2% annually, and a median-priced Australian home is $1 million, that’s $102,000 in paper gains in a single year, more than the median wage of $86,000.

Someone who owns a house earns more in appreciation than most of their neighbors make by going to work. Untaxed, unlabored, and unearned in any traditional sense.

But lots of investments rise by 10% per year. So why have ordinary Australians all become levered-up property investors by default? Why did having multiple investment properties become the norm?

For that, you need to understand negative gearing.

What is Negative Gearing?

In most countries, when you buy an investment property, you're on the hook for the P&L. If your mortgage costs $48,000 a year, but you only collect $36,000 in rent, then you take a $12,000 annual loss. That’s entirely your problem. You absorb the loss and hope the asset appreciates enough to make it worthwhile.

But not in Australia. Here, you can deduct that $12,000 loss against your personal taxes!

That's right — if you fall short, your taxable income drops, and your tax bill goes down. The government literally subsidizes your investment shortfall.

Think about the incentive here for a moment. Not only does this law encourage property investing, it encourages property speculation, as it rewards you most when your investment is losing money.

As long as your property appreciates more than your tax bill, you're coming out ahead.

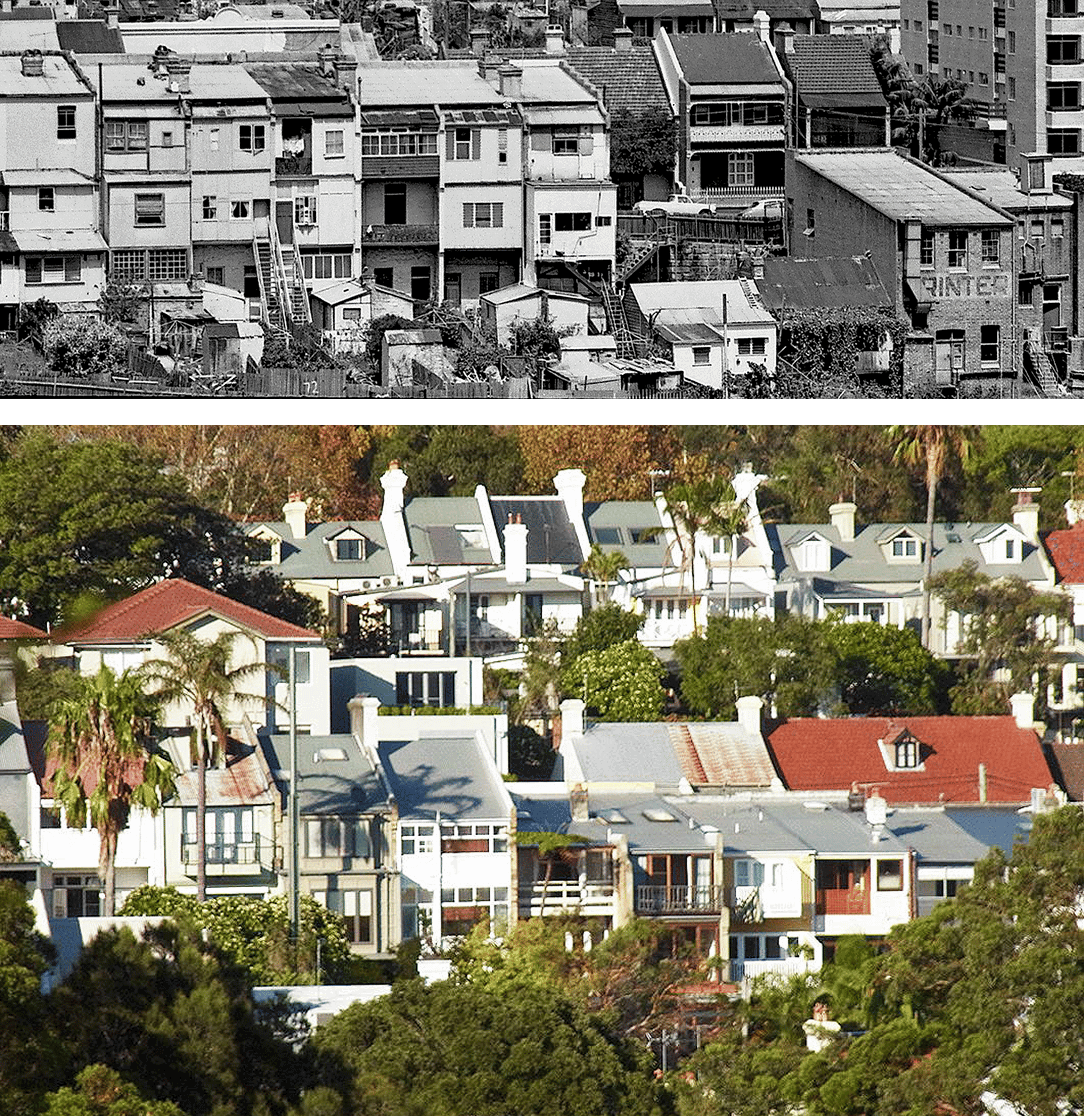

Negative gearing was created during the Great Depression as a way to encourage private investment in rental housing at a time when the government couldn’t build enough of it. The law is 90 years old. It predates television. Above: Sydney's Paddington used to be a housing commission suburb where the poor lived in terrace houses shared accommodation. Today it's one of the most expensive parts of the country.

When I first heard about how this worked, it blew my mind. In the US, rental losses can generally only offset rental income or other passive income. The idea of writing off a loss against your regular salary just doesn’t exist there.

To be fair, some countries do offer something similar. Canada, Germany, Norway, and Japan all allow rental losses to offset broader income to some degree.

But what makes Australia’s version uniquely powerful is the combination with something added later: a blanket 50% discount on capital gains for assets held longer than 12 months.

The aim was to encourage investment in Australian businesses.

Instead, billions more just flowed into housing.

And is it any wonder why?

Unlike investing in a business, you get to deduct real estate losses against your salary at your full rate, then pay tax on only half your capital gain when you sell! Maximum relief on the way down. Minimum exposure on the way up. What's not to love?

Personally, I'm torn on this concept. There’s something admirable about a tax system that gives teachers the same investment toolkit as finance pros. Most countries reserve these benefits for those who already have capital. Australia accidentally "democratized" property investing, making it extremely easy for anyone to speculate.

And they didn't even need to register as a business first. In some ways, that's a very good thing! After all, what is a "business," anyways? Should you really need special paperwork? We’re all a business, man.

The problem with Negative Gearing

The first problem is that this scheme has a huge price tag.

Last year, the tax subsidy from negative gearing cost the government $12.3 billion in foregone revenue. That's up 2x from a decade ago. It's become one of the fastest-growing tax expenditures in the country.

Second, most of that money flows upward. Yes, the system is open to everyone, but like most things, in reality the rewards scale sharply with income. 20% of income earners in the top tax bracket claim rental losses, compared to just 6% of those in lower brackets.

But in my opinion, the real cost is what this law does to capital allocation. When you give an entire nation a big fat reason to speculate on land, well, they'll speculate on land. Not on businesses or other productive assets. Land.

Even Esha, who has built his career in property and owns two investment properties himself, acknowledged the limits of it:

“I don’t strongly feel that investment property should be a thing that everyone does. At least not to the degree Australia has taken it.”

According to UBS, a whopping 55% of Australian wealth is tied up in real estate! Securities and other alternatives account for less than 10% — and that's with a world-class compulsory retirement system that forces diversification into equities! That's how powerful the gravitational pull of negative gearing has been.

Australia is a wealthy culture, yes. But it is not a diversified investing culture. Most marginal investment dollars just flow towards 'tried & true' real estate. As the CEO of an awesome alternative investing firm, this fact pains me.

But my pain is nothing compared to younger folks who are finding it nearly impossible to get on the property ladder.

Affordability is a massive problem here, as first-time home buyers compete against boomers with multiple properties who can easily negative gear their losses.

This law may have made sense during the Great Depression, but now it feels more like a loophole.

For decades, Australian politicians on both sides have known something needed to be done, but it was always the "third rail" of housing policy: too popular to touch.

There are 2.3 million Australians with at least one investment property, of whom about 50% are negatively geared — meaning the law directly affects roughly one in twelve people in the workforce.

But this figure understates the cultural weight, since these investors own a disproportionate share of rental stock, and drive outsized political influence.

So in my mind, I assumed reform would never actually happen.

Last month, the Albanese government proved me wrong.

Losses don’t disappear. They accumulate and can be used later, either when the property eventually turns profitable, or when you sell and crystallize a capital gain.

But the salary offset? Gone. Annual tax rebate? Gone.

If you’re losing $20,000 a year on a property at the top marginal rate, that’s roughly $9,400 you used to get back at tax time. Under the new rules, you have to pay the full $20k out of pocket every year until the asset makes money.

The 50% capital gains discount is gone too, replaced with inflation-based indexation and a 30% minimum tax rate on gains.

However, what really makes this change interesting are 3 big exceptions to the rule.

1) Existing property owners are grandfathered in

This is huge. Remember how I said I thought the government would never touch negative gearing?

Well, they found a way to touch it without actually touching it.

That's right: anyone who purchased a property before 7:30pm on May 12, 2026 is fully protected under the old rules.

Tax treatment, annual salary offset: all unchanged.

Imagine closing on one of these beauties on May 12 at 7:29pm and owing the government an extra $40k per year.

2) New developments are exempt

Second, the old laws are unchanged if you buy a newly constructed home.

The government’s logic here is simple: They want to incentivize developers to add to the housing supply, and they think incentivizing investors to scoop up their new builds (because they still get ridiculous tax breaks) will do it.

It makes sense in theory. This could redirect speculative capital away from established stock (which just shuffles ownership) and toward actual net new supply creation.

3) Self-managed retirement funds are exempt (!)

A few months ago, I mentioned that self-managed retirement funds are becoming incredibly popular in Australia.

These structures (known as Self-Managed Super Funds, or SMSFs) allow individuals full control over their own retirement funds.

Incredibly, SMSFs are explicitly excluded from the changes. Buy any property through your self-managed retirement fund and the new restrictions simply don’t apply to you.

Australia's wealthy have figured out there are huge tax advantages to investing in real estate through a self-managed fund. America's version is called the SDIRA, and you can get set up through IRA Financial.

Could this fix make things worse?

Esha and I agreed that grandfathering is the biggest problem here.

By freezing existing owners in place, you're effectively incentivizing them to never sell. After all, why sell a grandfathered property when doing so means your next purchase loses its tax advantage forever?

The reform designed to free up housing stock for owner-occupiers may, perversely, reduce the number of properties coming to market. The people supposed to benefit, first home buyers, are still competing for whatever’s left.

We have a similar dynamic in California, where the infamous Prop 13 capped annual tax increases at 2% as long as the owner holds the property. The moment they sell, the new buyer gets reassessed at current market value. This perverse dynamic means longtime owners pay a fraction of what new buyers pay in property tax, so they never leave.

The effect could be stark, permanently dividing Australian property investors into two classes: those who bought before the deadline keep the full subsidy indefinitely, and everyone else gets a fundamentally worse deal.

Esha, who owns two investment properties (and was planning a third before this new law) put it plainly:

"Properties basically never go down in value in Australia. This isn’t going to change that. All you’ve done is cut out the battlers.

The people most affected by this won't be the wealthy investors with five properties and a team of accountants. It'll be the $130,000-a-year couple in Melbourne who were stretching to buy in Ballarat [90 mins away].

It'll hurt the first-time investors who needed the annual tax rebate to make the cash flow work."

This is the deepest problem with the reform. It was designed to level the playing field. But in practice, it could just tilt the field toward those already inside the system (grandfathered owners) or those with enough capital to restructure their way around it (self-managed retirement fund owners).

Closing thoughts: Implications for Australia & beyond

I think the phasing out of negative gearing is a big deal, and I'm surprised it's actually happening.

At its core, this is about an inconvenient truth that every country eventually has to face: housing can either be a lucrative investment that goes up forever, or it can be affordable. It's extremely tough to do both. Personally speaking, I think any law that tries to tip the balance toward affordability is noble.

But putting my personal thoughts aside, it's important to remember that The Lucky Country is the second wealthiest nation on earth by median wealth. It ranks sixth in ultra-high net worth investor growth, and ranks fourth in billionaire growth.

It also has, by design or by default, the most property-heavy wealth profile of any major economy on earth.

For the first time in as long as I can remember, the question of what to do with ~$200k in the bank doesn't have an easy answer. The “just buy property” mantra suddenly requires an asterisk.

So where does all this Aussie investment capital go instead?

Well, if you're a fund manager or investment platform already targeting Australian investors: the timing has never been better.

The most government-incentivized thing Australians have done with their money for ninety years just got meaningfully less attractive. That capital has to go somewhere. Film financing. Rare earths. Wine and spirits. Classic cars. Asset classes that don’t make the front page of the Herald Sun every Sunday but have been delivering quietly for years.

For those not yet targeting Australian investors, I have some advice:

Start now.

This is one of the wealthiest populations in the world, with a deeply ingrained habit of allocating almost everything to a single asset class. And suddenly they're looking for new options.

"Personally, I don’t think this is 'the end' of property investing. But it definitely changes how Aussie investors will assess deals moving forward." — Esha Frykberg

My take? This law is right in spirit but messy in execution.

The idea that we shouldn’t incentivize an entire nation’s investment capital into a single (unproductive) asset class for ninety years straight is sound.

But the grandfathering and SMSF carve-out are imperfect. It'll help some people it was designed to help. It'll hurt some it wasn’t. And it'll take years to know which is larger.

In the meantime, as an alternative asset manager I'm beyond delighted to see Australian capital start getting put towards more productive areas of society.

If you’re an accredited investor reassessing your allocation, well, Altea is the best place to start.

---

That's it for today!

Big thanks to Esha Frykberg for the boozy but interesting discussion. 🍻

Until next time, Stefan

Disclosures

This issue was written and edited by Stefan von Imhof

This issue was sponsored by IRA Financial.

Alt Assets, Inc has no current holdings in any companies mentioned in this issue.

Stefan is a negatively-geared Australian property owner who is (luckily) grandfathered in.

Recent emails from Alts

Shop without the noise

Get our free newsletter of hand-picked sales you need to hear about from the web's best brands.

There was a problem subscribing this email address

Good stuff coming your way!

ProTeam

Your account is managed by your organization. Contact your administrator for access to Pro features.