In the world's most desirable cities, housing supply never seems to outrun demand. The culprit may be the agglomeration loop.

Welcome to the Alts Sunday Edition 👋

I was visiting Hong Kong last month, and I couldn’t get over the real estate prices.

Hotel rooms the size of a San Francisco closet are priced like the Ritz-Carlton. Residential towers are stacked so tight you could reach out and touch your neighbor’s laundry.

On the flight back, the same question kept turning over in my head: why?

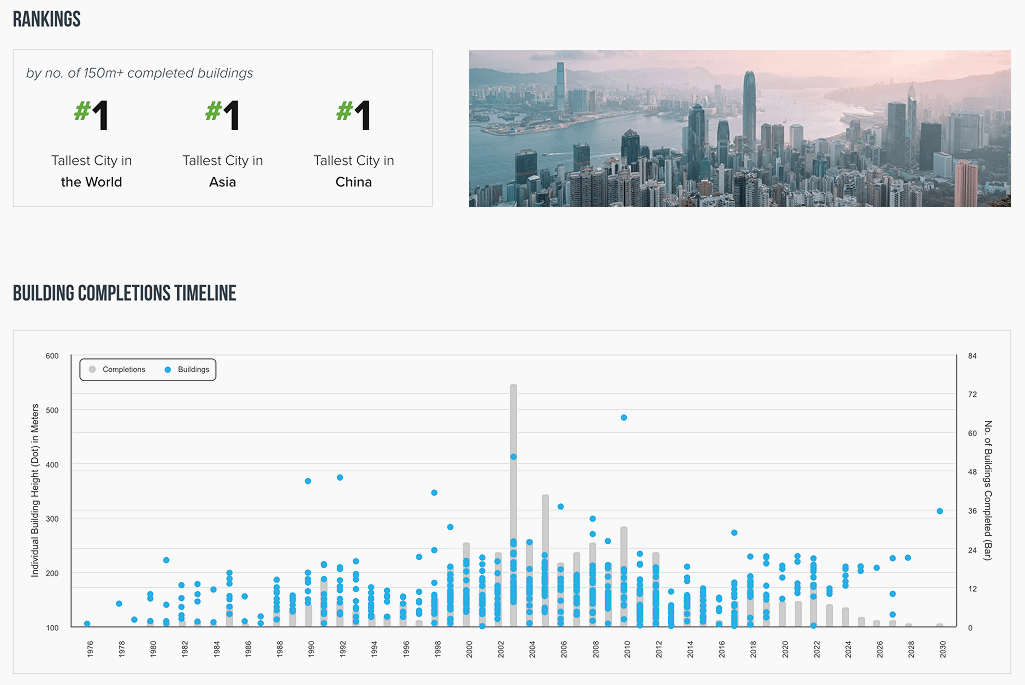

After all, Hong Kong has more skyscrapers than almost any city its size. It's one of the densest urban skylines on earth. They’ve been building nonstop since the early 70s.

And yet somehow, no matter how many new units go up, prices never seem to come down.

A few days later I was in Malaysia with Wyatt — someone who has a considered opinion on every economic concept you can throw at him.

So I thew the question at him: Why does Hong Kong housing seem to completely defy supply and demand?

He thought about it, and said he said he wasn’t sure.

I’ve been thinking about it ever since.

Today I want to explore exactly that question. Why is it that building more housing doesn’t always make housing cheaper. It’s a genuinely unsettled debate. The smartest economists in the room can’t fully agree on any of this, and I sure as heck don’t have a clean answer.

But I think it boils down to two concepts:

Induced demand, which is the same force that explains why building more freeways doesn’t fix traffic, and

Agglomeration effects, which may explain why successful cities generate demand faster than they can build supply

In this issue, I'll explain why I've become a housing supply skeptic.

Let’s go. 👇

🇪🇸 Invest in the rental market Spain never built

Valencia, Spain has become one of Europe's best rental markets.

Our co-founder Wyatt lives 40 minutes down the coast (in Jávea) and has been watching this market run wild for years. Property prices are up 117% since 2019, and 24% of rentals in Valencia are leased within 24 hours.

As he explained, this is happening because Spain was structurally built never to have a rental sector, and now desperately needs one.

For our second Real Estate SPV, we're investing in Álvaro López: a 16-unit residential building in La Malva-rosa, Valencia's beachside district, steps from the Mediterranean.

This will be our second Real Estate SPV. Deal Memo will be published next week.

Details

Here's what the rough structure looks like right now:

36 month estimated timeline

8% fixed annual coupon + 25% profit share on net proceeds

Projecting a ~10.1% XIRR

Minimum investment of €7,500 (1 token)

Pre-sale deposits protected under Spanish banking law, held in bank escrow

How investors are protected

Five regulatory layers: ERIR, ESI, Notary, Commercial Registry, and CNMV registration.

Capital stack: Sponsor equity is subordinated below investor capital. Senior bank → token holders → sponsor.

Fiduciary trustee: A dedicated Bondholders' Representative acts on behalf of investors throughout the entire investment lifecycle.

No trade creditor risk: Construction is financed on a progress basis. Payables are settled as work advances, so no creditor stack accumulates against the issuer.

Valencia meetup July 9

We're also planning a site visit and cornerstone ceremony on July 9. Guy Kleinboim will walk us through the site, followed by a delicious beachside paella lunch. 🥘

This is a potential Altea SPV for accredited investors. Non-accredited investors can also express interest and invest directly via Brickken.

The freeway metaphor

In the 1960s, urban planners had a theory: traffic is bad because there aren’t enough lanes. Build more lanes, more cars fit, congestion eases. Simple supply and demand, right?

Well, it didn’t work. A landmark 2009 study by transportation researchers Duranton and Turner found that vehicle miles travelled expanded in near-perfect proportion to the roads built to accommodate them. Every new freeway lane filled up, and sometimes it made congestion even worse.

Researchers gave this phenomenon a name: induced demand. It's the idea that new supply doesn’t just serve existing demand, it creates demand that wouldn’t have existed otherwise.

It’s one of the most counterintuitive and well-documented findings in urban planning. And once you see it, you can’t unsee it.

With 26 lanes, Houston's Katy Freeway is the broadest highway on earth. A $2.8 billion expansion in 2008 was supposed to end the congestion. Within a few years, morning commute times had increased by 30% and afternoon times by 55%. The road had built its own traffic. Researchers call this induced demand, later dubbed the "fundamental law of road congestion."

Supply skepticism

So here’s the question I keep coming back to: what if the same thing is happening with housing?

The conventional wisdom held by mainstream economists and YIMBY activists is that housing is expensive because we don’t build enough of it. Build more, and prices will follow.

And look, that logic isn’t wrong! In markets with relatively contained demand, it clearly works.

But a small group of serious researchers have started pushing back on the idea that supply alone can solve the problem in the world's most in-demand cities.

Academics at NYU’s Furman Center have given this position a name: supply skepticism. The idea is that even if new housing brings prices down temporarily, it may also signal to the world that a city is open, growing, and worth moving to. This signal attracts new demand that eventually swamps whatever supply was added.

In 2020, Andrés Rodríguez-Pose of the LSE and Michael Storper of UCLA published a provocative paper in this space, arguing that the affordability crisis in major cities has less to do with zoning restrictions than with decades of rising income inequality and the return of high-wage jobs to urban centers. They argued that building more housing mostly serves the affluent, and may do little for everyone else.

In other words, "Build it, and they will come. And come. And come..."

When building more has worked

This all raises an obvious follow-up question: are there cities where building more housing actually succeeded in bringing prices down?

The answer is yes, absolutely. Sometimes, building more really does work.

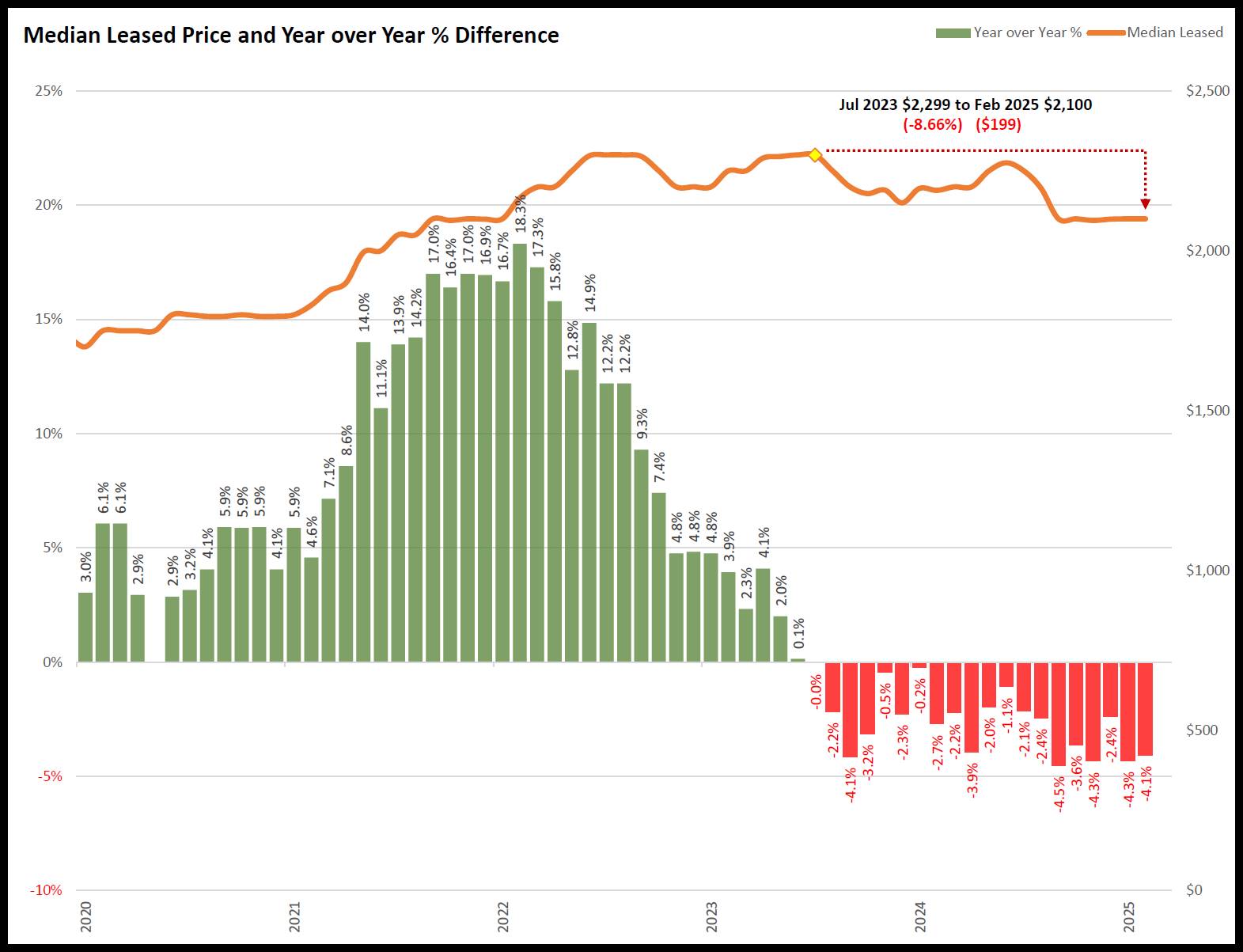

Austin, Texas has become the poster child for YIMBY success. In the early 2020s, the city went on a construction tear, adding tens of thousands of new units. By 2023, it was one of the only major US cities where rents were actually falling — in some cases by double digits.

Tokyo is the other case everyone points to. Over the past 50 years, the city nearly tripled its housing stock while its population kept growing. Rents barely moved. The secret a 2002 law that effectively stripped local governments of the ability to block new development.

Rent prices in the Austin metro area have been decreasing since 2023. A massive post-covid construction boom oversupplied and effectively stabilized the rental market. Chart courtesy of Teamprice

So yes, the model works under the right conditions! But every city has unique characteristics working both for and against price stabilization.

Austin is a sprawling Sun Belt city with room to grow and no special mystique pulling wealthy people towards it. And Japan’s population is shrinking, which puts a natural ceiling on demand.

But the fact remains that, when you look at most cities that have an enormous baseline of demand (New York, San Francisco, Sydney, Hong Kong, London, Singapore) the supply responsenever seems to be enough.

Something else is going on here, and that something has a name: agglomeration.

The agglomeration loop

Economists have thoroughly modeled how markets respond to scarcity. What they have not adequately grappled with is the fact that cities don’t just house people, they generate economic gravity.

Agglomeration is the term for the self-reinforcing cycle that happens when people and businesses cluster together. Proximity creates productivity. Productivity creates wages. Wages attract more people. More people create more amenities — better restaurants, better hospitals, better universities, better job markets. Better amenities attract even more people. And so on.

By the way, this is all a feature, not a bug. It’s actually why cities exist in the first place!

For most of human history, people clustered together out of pure economic logic. Merchants settled near ports because that’s where the trade was. Craftsmen set up near other craftsmen because shared knowledge made them all better at their work. Financial centers emerged where capital was already concentrated.

Venice, Wall Street, Victoria Harbor, and Las Vegas are the natural result of proximity compounding. Once a place develops a critical mass of talent, capital, and opportunity, it creates its own stickiness, its own moat, its own form of gravity. Painting by Gaspar van Wittel, Public Domain

This is what I see happening in the world's most desirable cities. When you build more housing in a city like Hong Kong or San Francisco or London, you’re just feeding this loop. More residents means more economic activity, more amenities, more desirability, and more demand for housing from the next wave of people who want in.

The supply response seeds its own demand. And there's no natural force to stop the cycle.

The agglomeration loop explains why building more housing in the world's most desirable cities can paradoxically sustain or even accelerate demand. Each new resident makes the city slightly better at being a city.

Harvard economist Edward Glaeser has documented exactly this dynamic. In highly productive cities, rents rise faster than wages precisely because demand for urban amenities compounds over time. The city gets better at being a city faster than it can build housing for everyone who wants to live there.

Hong Kong is the most extreme illustration of this loop running unchecked. The price-to-income ratio (i.e., how many years of median salary it takes to buy a home) has gone from around 4–6x in the 1950s and 60s to nearly 29x today. They never stopped building, but they could never get ahead of the loop.

The uncomfortable implication of all this is that in the world’s most desirable cities, the agglomeration effect may simply be stronger than any supply response a functioning democracy could realistically produce. You’d have to build faster than the city’s own gravity pulls people in. And the more desirable the city, the faster that gravity pulls.

Is building more housing worth it?

Let me be clear about something: I’m not arguing that building more housing is pointless. It definitely helps. All else being equal, more supply is better than less!

But "all else being equal" almost never applies in the cities where housing affordability is most desperately needed.

I think Rodríguez-Pose and Storper nailed it: When you have a city that is simultaneously becoming more productive, more amenity-rich, and more globally desirable, you are not facing a simple supply problem. You are facing a demand problem that compounds faster than supply can chase it.

The honest implication here is that, in the world’s most desirable cities, no realistic amount of building may be sufficient to stabilize prices.

Sure, prices can come down via other mechanisms (lower population/immigration, rezoning, adjusting taxes/incentives, etc). But not by new supply alone.

I don't mean to be defeatist, but when I look at the world's most desirable cities, that's the conclusion I've come to.

Closing thoughts: What could actually reduce housing prices?

Anyone who tells you confidently that they’ve solved the housing affordability puzzle is either selling something or hasn’t thought hard enough about it. This is a genuinely stubborn complex problem that resists simple fixes.

But there's one idea that doesn’t get nearly enough mainstream attention: the land value tax (LVT).

The concept goes way back to the 1800s, when economist Henry George argued that the value of land is created not by its owner but by the surrounding community. Neighborhood, infrastructure, amenities, agglomeration.

George realized that a property owner who sits on a valuable plot in central Hong Kong or San Francisco didn’t create that value, the city did. George’s argument was that taxing land value, rather than buildings or income, would discourage speculative land hoarding and encourage development. Use it or lose it, essentially.

The idea never went away. Contemporary economists including Joseph Stiglitz and research from the Lincoln Institute of Land Policy have argued that a well-designed LVT could simultaneously dampen speculative demand, encourage more efficient land use, and generate public revenue without the distortions that other taxes create.

As our very own Brian Flaherty pointed out in Parking Lot Economics, some of the most unaffordable cities on earth are sitting on vast amounts of underutilized land held by owners waiting for values to rise further. A land value tax would directly change those incentives.

It’s not a silver bullet. No single policy is. But it’s the kind of structural intervention that actually addresses the root of the problem rather than chasing the symptoms.

For now though, I sit with the idea that the cities we’ve built may simply be too good at their own job — generating the kind of gravity that no amount of construction can fully outrun.

That’s not a reason to stop building, but it's an opportunity to be honest about what building actually does.

And maybe to think harder about the land underneath. 🌆