👉 At a glance: Preferred equity SPV | Min $10K | Target $1M | First mission Q3 2026 | Priority dividends + equity upside

Hey folks,

For the past few weeks, we’ve been talking a lot about Japanese whisky.

Today, I'm happy to announce our due diligence is complete and the investment memo is ready.

Whisky I is our investment in a diversified portfolio of Japanese whisky casks, sourced in partnership with dekantā, the world’s largest platform for Japanese whisky.

The strategy is simple but powerful: buying at the cask level and selling at the bottle level, capturing the wholesale-to-retail spread in a supply-constrained market.

We are genuinely excited about this one. It combines scarcity, brand-driven pricing power, and a clear path to liquidity through staggered releases.

I think you’ll find it as compelling as we do.

Note: Full Memo Access is Restricted to Accredited Investors

We have prepared a comprehensive deal memo with detailed analysis and full disclosures.

However, due to regulatory and compliance requirements, we can only provide the complete memo to individuals who have self-declared their accredited investor status.

Once completed, our team will review and send you the full deal memo.

In the meantime, you can explore the redacted overview below to get a sense of this opportunity.

📌 Details

Deal Name: Japanese Whisky Cask Vertical (Whisky I)

Asset Class: Physical Japanese whisky casks

SPV Entity: Alt Assets LLC (Series 12)

SPV Sponsor: Altea

Sourcing Partner: dekantā (Tokyo, Japan)

Target Raise: ~USD $515,000

Minimum Investment: USD $10,000

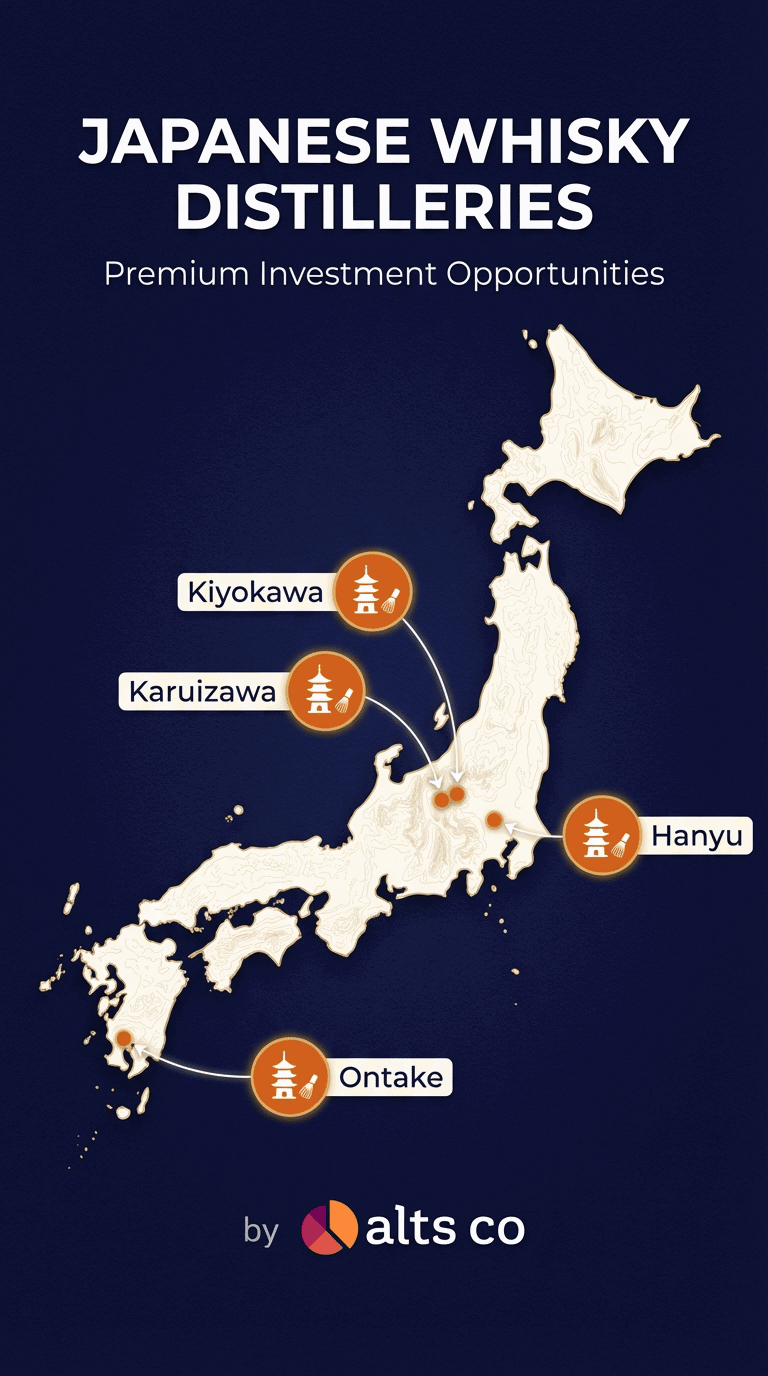

Portfolio: 11 casks across 4 distilleries

Hold Period: Staggered: first exit mid-2026, final 2033

Distributions: Annually, as casks are bottled and sold

Summary

Japan's whisky industry operates nothing like Scotland's.

Distilleries are vertically integrated.

They don't share stock.

They don't use third-party warehouses.

Production volumes at the craft level are tiny: we're talking 400 to 1,800 casks a year, total.

And ownership documentation comes directly from the distillery, not from a broker or intermediary.

That changes the risk profile entirely.

Whisky I is a portfolio of eleven casks across four distilleries -- Kiyokawa, Hanyu, Ontake, and Karuizawa -- with staggered bottling dates from mid-2026 through 2033.

You buy at wholesale cask prices, exit at retail bottle prices through Dekanta's global e-commerce platform (400,000 customers, 39 countries), and receive annual distributions as each cask is bottled and sold.

Market

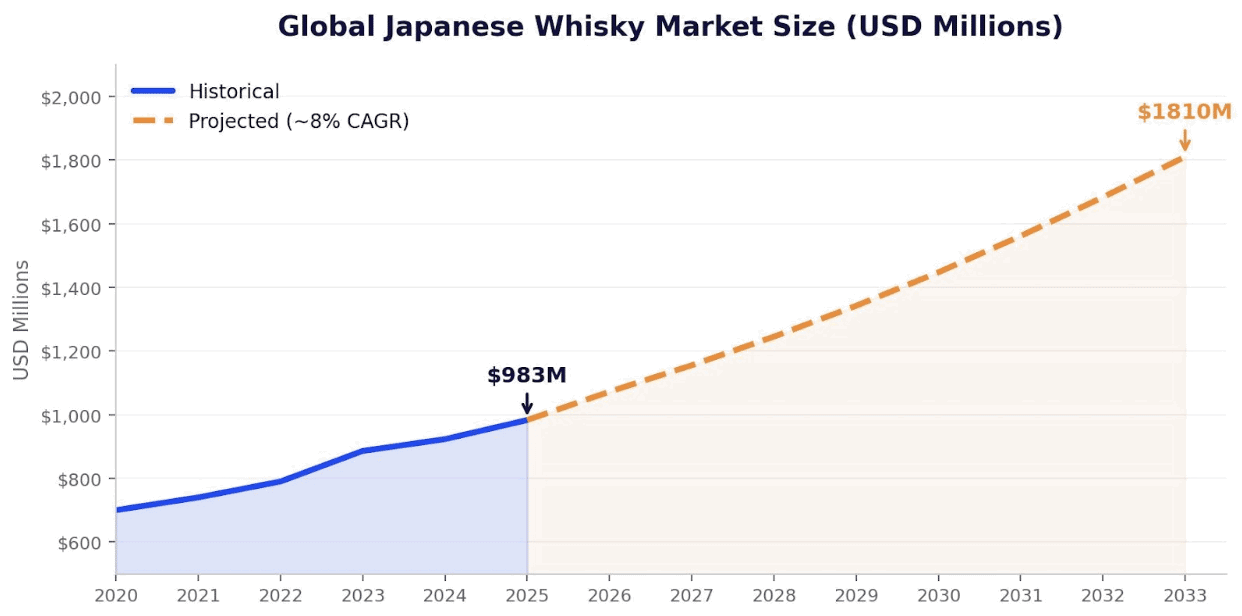

The global Japanese whisky market was valued at approximately USD 983 million in 2025 and is projected to exceed USD 1.8 billion by 2033 (~8% CAGR).

Japanese whisky exports reached 43.6 billion yen in 2024, accounting for 34.6% of all Japanese alcoholic beverage exports. Over 120 distilleries are now operational, up from ~70 a decade ago.

The craft segment operates on a vertically integrated model unique to Japan: distilleries produce, mature, and bottle their own whisky. Production at craft distilleries is deliberately limited to 400–1,800 casks per year, creating genuine supply constraints that support premium pricing.

Source: Grand View Research, Global Growth Insights, industry estimates. Historical data to 2025; projections at ~8% CAGR.

Projected annual cash flow

Why does whisky fit in your portfolio?

If you've been reading our recent work on geopolitical risk — the Strait of Hormuz closure scenarios, the metals and commodities repricing, the tariff regime uncertainty — you'll know we've been spending a lot of time thinking about portfolio resilience.

Physical whisky casks sitting in Japanese mountain distilleries have approximately zero correlation to any of that. They don't care about oil prices, semiconductor export controls, or what the Fed does next quarter.

That's not an accident.

This asset class is driven by a completely different set of variables: Japanese craftsmanship culture, global collector demand, supply constraints at the distillery level, and time.

The whisky matures regardless of what happens in equity markets. The scarcity is structural, not cyclical. And the exit channel — retail bottle sales to whisky enthusiasts and collectors — is about as far from a macro trade as you can get.

For most portfolios that are already heavy in equities, real estate, or even other alts like film finance, adding an uncorrelated physical asset with a defined exit schedule and tangible collateral is a sensible diversifier.

It won't move the needle on its own, but it's the kind of position that holds its value precisely when everything else is getting interesting.

Frequently Asked Questions

What exactly am I investing in?

A portfolio of eleven physical whisky casks stored at four distilleries across Japan. The SPV owns the casks; you own a proportional share of the SPV. Net proceeds from bottling and sales are distributed annually.

Why Japanese whisky and not Scotch?

Japan’s vertically integrated model means casks stay at their distillery with direct ownership documentation. Production is a fraction of Scotland’s. Retail prices are structurally higher.

How do I know the casks are real?

Ownership certificates are issued directly by each distillery and recorded on their warehouse ledger. Cask owners can visit, inspect, and sample. Altea conducts annual verification visits.

Who is the legal owner of each cask?

The SPV/Altea is the full and legal owner, reflected on each distillery’s warehouse ledger. Ownership certificates are signed by the distillery owner and Master Distiller and shared with the SPV following payment. Casks are stored onsite at each distillery’s warehouse alongside the distillery’s own stock.

What happens to the casks if dekantā ceases to operate?

The SPV/Altea is the legal owner of the casks on the distillery’s warehouse ledger, so there is no counterparty risk with dekantā. In the event dekantā ceased operations, investors would have a direct relationship with the distillery for support, bottling, and resale. Cask ownership can also be transferred at the owner's request, a straightforward administrative process.

Can casks be sold before bottling?

Yes. Dekanta maintains the world’s largest network of cask buyers. Base case assumes holding to bottling for maximum value.

What insurance covers the casks, and what if a cask is damaged or lost?

If a cask is damaged through leakage or breakage, the distillery will replace it with a cask of the same yield and vintage from distillery stock. Casks are stored alongside distillery stock and receive the same meticulous care. The Purchase Agreement also contains a standard force majeure clause covering catastrophic loss scenarios.

How are management fees charged?

Year 1: 2% on committed capital. Year 2+: 2% on remaining AUM (net asset value of unsold casks), deducted from distributions. You stop paying fees on capital that has already been returned to you.

Why is the XIRR so high?

The wholesale-to-retail spread is 4–5x, and nearly half the capital returns within 12 months. The early exits compress the effective holding period for most of the portfolio.

What if Karuizawa underperforms?

Even at half the projected price (USD 625/bottle), the Karuizawa cask returns ~USD 133,000 net to SPV, a 1.36x on that single cask. The portfolio does not depend on Karuizawa hitting its target.

How are distributions calculated?

Gross bottle revenue − dekanta 20% − bottling − shipping = net to SPV. SPV deducts the management fee (from year 2, on AUM) and distributes the remainder pro rata. Carry on cumulative profits after return of capital.

Who decides when to bottle, and can bottling be delayed if market conditions are weak?

Cask owners are the ultimate decision-makers on bottling timing, provided the whisky meets minimum age requirements (3 years for most distilleries; 10 years for Karuizawa). The bottling windows in the deal are structured to provide staggered returns, but investors can choose to mature casks longer or bottle earlier if conditions warrant. Dekantā provides ongoing market guidance but does not have final say.

Is there a secondary market for casks or SPV interests?

Yes, on both fronts. Dekantā operates an active cask marketplace with a global client base across 29 countries and over 300 cask owners, providing a natural buyer pool for any resale. There is also a secondary market for fractionalised SPV interests, as demonstrated by dekantā’s partnership with Rally, which IPO’d five Karuizawa casks for over USD 600,000.

What does the downside scenario look like?

Even in the most conservative scenarios, projected returns remain competitive given the premium associated with acquiring whisky at the cask stage. In most downside cases the issue tends to be timing rather than permanent value loss: if market conditions are weak at a planned bottling window, the whisky continues to mature in cask, which historically supports long-term value. This flexibility is distinct from categories like tequila where maturation windows are shorter and bottling schedules are less flexible. Japanese whisky can also be released younger or held longer than Scotch, giving additional optionality.