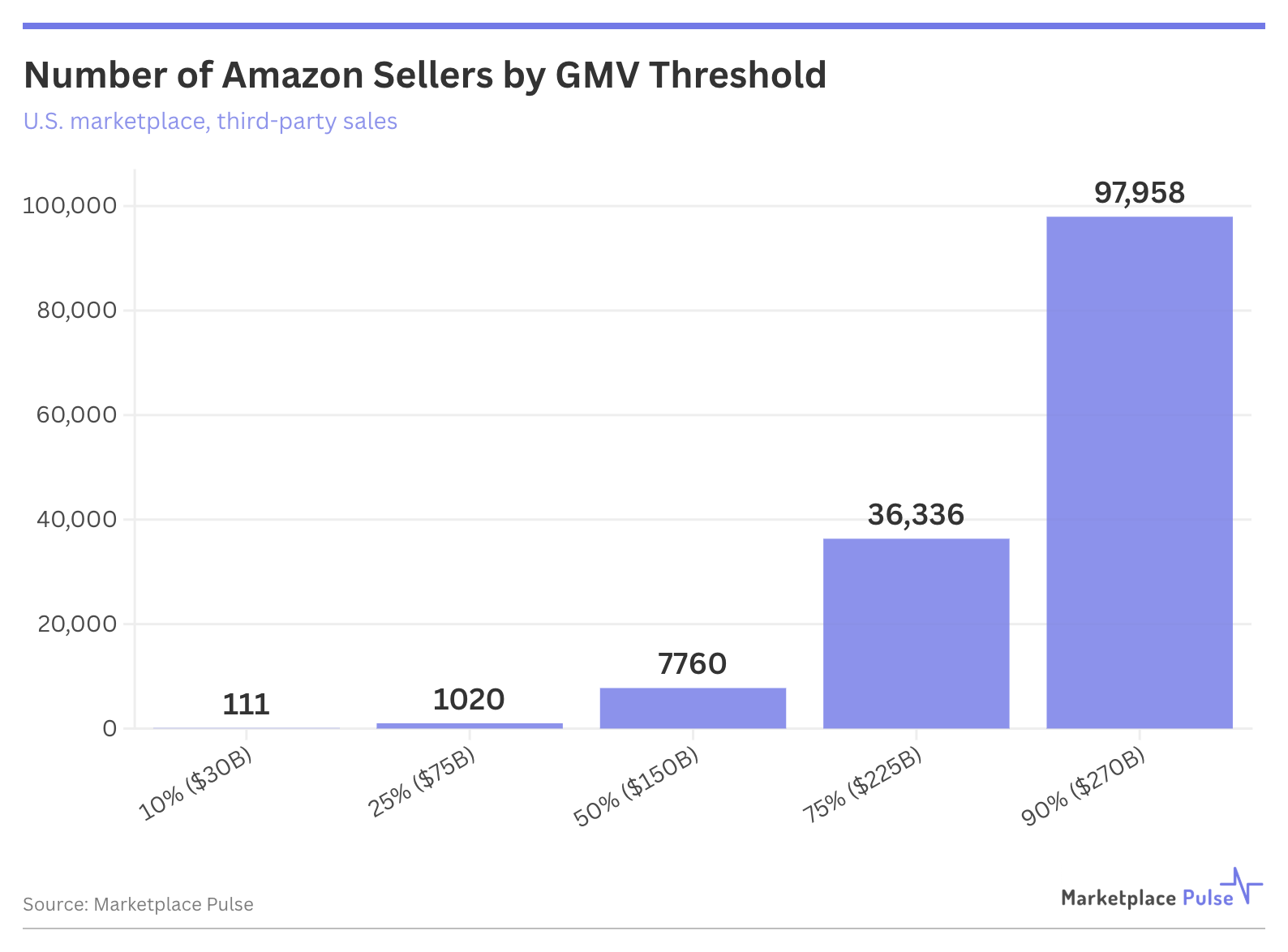

The shift reflects top sellers capturing growth disproportionately - while the seller count within the cohort halved, the GMV at the 50% threshold increased from approximately $115 billion to $150 billion, with average per-seller revenue in this cohort more than doubling to nearly $20 million annually.

U.S. sellers dominate at this scale, representing 55% of these top sellers while controlling 67% of their combined GMV.

Chinese sellers account for 41% of the cohort but generate 30% of GMV, demonstrating that American sellers maintain significantly higher per-seller revenue at the top end of the marketplace.