Welcome to Titan’s Take, our POV on the latest.

|

|

|

"Wall Street indexes predicted nine of the last five recessions." Paul Samuelson (Nobel Prize-winning economist)

We loosely pay attention to macro forecasts. Predicting short-term macro environments is a fool's errand more often than not, but we keep an eye on what people are saying in case there's signal in the noise.

Finding it usually requires not reacting to the headline, but hunting for the second-order conclusion hiding underneath it.

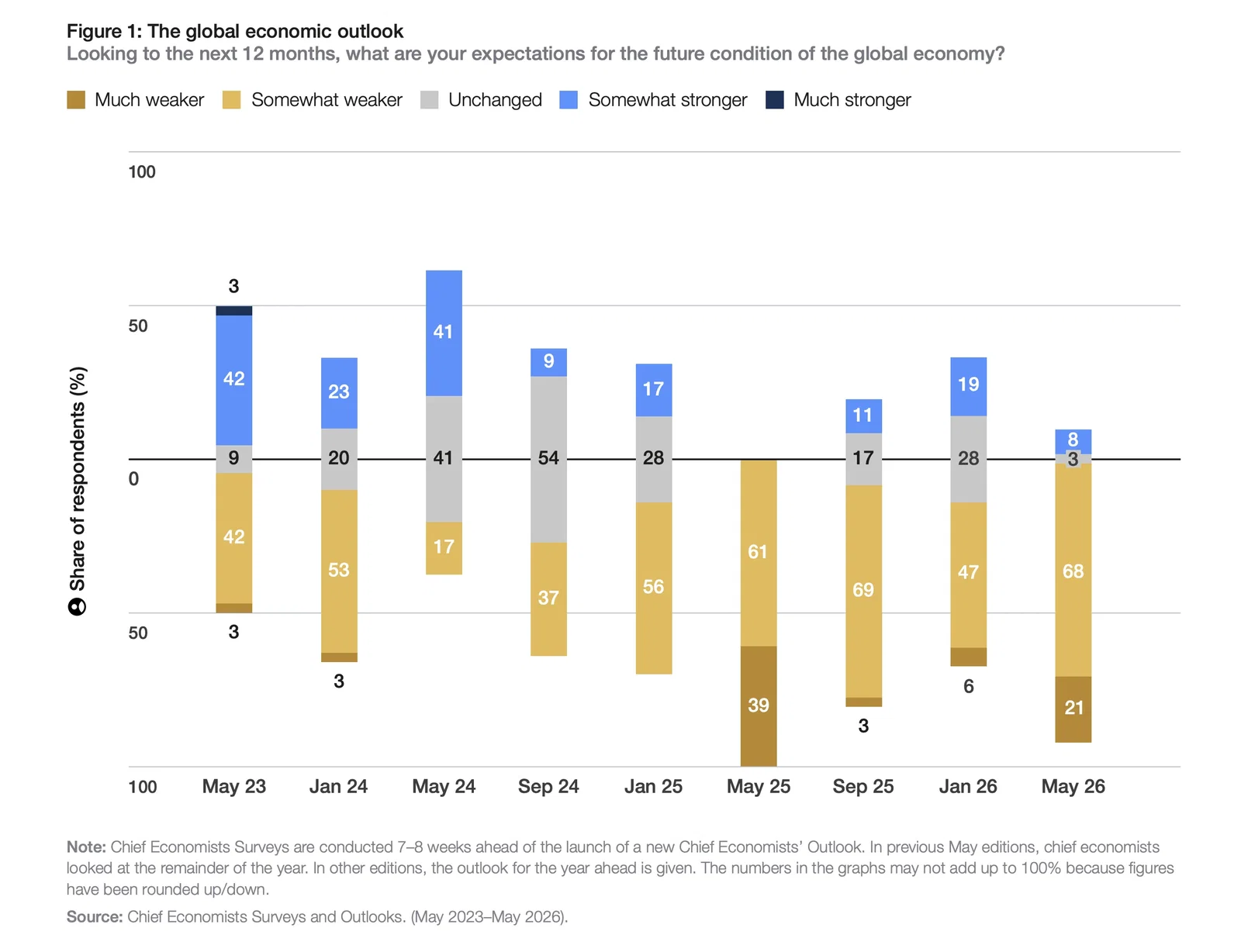

So when 89% of the world's top economists expect global growth to slow over the next year, but only 13% think an actual recession is coming, that gap is the whole story.

The World Economic Forum's Outlook landed this week. First-order read: grim. Escalating conflict in the Middle East, the Strait of Hormuz closure, 94% of economists projecting rising inflation. If you stopped there, you’d be a bit nervous.

|

Source: World Economic Forum |

Second-order read: the world's top economic minds are not calling for a collapse. What they're describing is divergence.

The Middle East is bearing the brunt, Europe faces real stagflation risk as energy shocks compound, but the U.S. and India are projected to hold strong growth, insulated by domestic demand and capital investment that doesn't depend on a functioning Strait of Hormuz.

Global capital is already moving. Big corporations are relocating supply chains out of volatile zones and into the U.S. and India at a pace the WEF describes as synchronized and significant.

That's not a projection. That's companies making operational decisions in real time, with real money (feet on the street, not just forecasts).

One other thing buried in the report: AI optimism is cooling at the edges. 92% of economists still expect adoption to surge, but the timeline for productivity gains outside of tech and digital has stretched. Construction, engineering, healthcare…the legacy industries where AI was supposed to transform margins are taking longer than the 2024 consensus assumed (worth watching).

The spread between first and second-order conclusions always widens during volatility. The U.S. large-cap equities we hold in Flagship, and the ones that make up the S&P 500, generate revenue globally and carry the balance sheet flexibility to withstand regional shocks.

Right now, boring is working. The U.S. is where global capital wants to be.

|

|

|

From Giovanni Tiso, CFP®, Lead Financial Planner at Titan:

"For the long-term compounding bucket, the money you're not touching for years, short-term macro noise shouldn't drive the strategy. Bucketing matters: near-term money shouldn't ride on next quarter's market, and long-term capital shouldn't care about it.

That foundation should be diversified across U.S. equities, international markets, fixed income, and alternatives where applicable, primarily weighted toward the U.S. and the forward progress of its economy. Layer in direct indexing for tax efficiency (Titan Direct Indexing coming soon), and for active alpha exposure, Titan Flagship.”

|

|

|

Titan Global Capital Management, Inc.

PO Box 4668 | PMB 85274

New York, New York 10163-4668 US

© 2026 Titan, All rights reserved.

|

Advisory services are provided by Titan Global Capital Management USA LLC ("Titan"), an SEC-registered investment adviser. Titan’s affiliate, Titan Global Technologies LLC (“TGT”), is an SEC-registered broker-dealer. Both Titan and TGT are subsidiaries of Titan Global Capital Management, Inc. This content is for informational purposes only and is not investment or financial advice, tax or legal advice, an offer, solicitation of an offer, or advice to buy or sell securities or other products offered by Titan, TGT, or any third party. Any mention of companies, securities, asset classes, or investment strategies does not constitute affiliation, an endorsement, or a recommendation.

References to investment themes are based on Titan’s internal research and opinion as of the date of this communication. Any descriptors used should not be construed as a promise of quality or a guarantee of performance. Statements made in these communications represent opinions and conjecture, and should not be construed as a guarantee of future results. This communication may contain forward-looking statements, which are subject to inherent risks and uncertainties that could cause actual results to differ materially. They should not be relied upon when making investment decisions. We do not undertake any obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events, or otherwise.

References to specific stock performances are provided for historical market context and are not indicative of future results or the performance of any Titan strategy. Any performance mentioned regarding individual securities reflects market performance for educational purposes only and is therefore shown gross of fees, where applicable. Actual performance may vary based on individual circumstances, including the specific timing of trade execution, which can impact the cost basis of any given investment. Valuation assessments in our communications are based on internal analysis and are for informational purposes only. They should not be the sole basis for investment decisions and may differ from others' views or assessments. No warranty is made regarding their accuracy or completeness. The mention of a security does not imply it is held in a Titan strategy. Where Titan does hold a company mentioned in our strategies, we’ll disclose it.

Various Registered Investment Company products (“Third Party Funds”) are offered by third-party fund families and investment companies on Titan’s platform as one of many potential investment options available to Titan’s clients, that may or may not be recommended based on an individual client’s investment objectives, risk tolerance, or suitability. Third Party Funds that are available on Titan’s platform are interval funds, which are highly speculative and subject to a lack of liquidity compared to other types of investments. Always review the prospectus in its entirety for a full list of risks associated with investing in the Third Party Fund before making any investment decisions. Liquidity and distributions are not guaranteed, and are subject to availability at the discretion of the Third Party Fund.

All investments involve risk, and the past performance of a security, particular strategy, or financial product does not guarantee future results or returns. Investment growth is not guaranteed. No strategy or asset guarantees the accumulation of wealth, and any potential benefits are subject to market, tax, and individual financial risks. Certain investments are not suitable for all investors. Diversification is a portfolio allocation strategy that seeks to minimize inherent risks by holding assets that are not entirely correlated. Keep in mind that while diversification may help spread risk, it does not ensure a profit or protect against loss. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. There is always the potential of losing money when you invest in securities or other financial products. Investors should consider their investment objectives and risks carefully before investing. The price of a given security may increase or decrease based on market conditions and clients may lose money, including their original investment and principal. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. Investment decisions should be based on individual financial circumstances, objectives, and risk tolerance. Investments in securities are not FDIC insured. Please visit www.titan.com/legal for additional disclosures.

|

|

|

|