Welcome to Titan’s Take, our POV on the latest.

|

|

|

If you've been waiting on the Fed to cut rates, this week ended the wait. The cut policymakers had penciled in for 2026 is gone. The Fed's own projections now lean toward a hike instead. And its new chair just made the next move harder to read than it's been in years.

Kevin Warsh ran his first meeting since succeeding Powell in May. The Fed held rates at 3.5% to 3.75%, the fourth straight hold and the least interesting thing that happened. Warsh gutted the policy statement to a few lines, skipped his own rate forecast, hinted at fewer press conferences, and stood up five task forces to rethink how the Fed operates, communications and the dot plot included. His point: more than a decade of telling markets what it planned next had turned prices into a mirror, just reflecting the Fed back at itself. So he's taking the megaphone away, on purpose, and asking markets to read the economy instead of him.

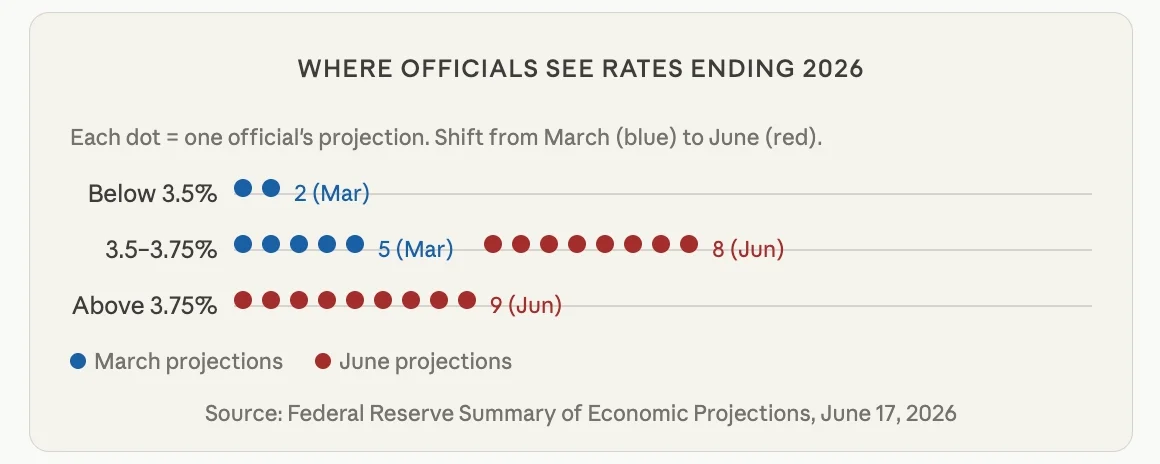

The dot plot

The dot plot shows where each of the Fed's 19 policymakers expects rates to go. Three months ago the median pointed to a cut. Wednesday it flipped: the median now sees rates ending 2026 at 3.8%, up from 3.4% in March, with nine of 18 officials above the current range. One dot was blank, widely assumed to be Warsh's, fitting a chair who has long argued forward guidance ties the Fed's hands. Behind the hawkish turn: May inflation ran 4.2% year over year, the hottest since April 2023, on an energy spike tied to the Persian Gulf conflict.

|

What the bond market said

Bonds got the message fast. The 2-year Treasury yield, the cleanest gauge of rate expectations, jumped 16 basis points to 4.21%, its highest in over a year. Equities finished lower, tech leading, and CME futures now put October hike odds near 61%.

What it means for you

Does this reach your accounts? In a few quiet ways. The cheaper mortgage or refi some have been waiting on looks further off. Cash and short-term bonds keep paying well, a plus for savers, though 4.2% inflation still outruns most of those yields. And the rate-sensitive growth stocks that get marked down when rates stay high are the same names that dominate most index funds: Nvidia, Microsoft, Meta, and Alphabet together make up more than 30% of the S&P 500. A quieter Fed adds one more thing, more volatility, since fewer signals mean more surprises.

Our view

Do you need to act? For most people, no. Trading around a single meeting is how investors turn volatility into losses. What's worth a look is whether your portfolio quietly leans on the names most exposed to rates, often through an index fund where a handful of AI giants do the heavy lifting, rather than by choice. We'd rather own quality businesses with real pricing power that don't depend on cheap money, and the AI buildout itself is gated by physical capacity, not the funds rate. The real swing factor from here is energy: the 4.2% print leaned on oil, which already softened this week on Persian Gulf peace signals. That shapes the next few meetings more than anything said at a podium.

Happy Friday,

Titan Team

|

|

|

A note from Aahana Chatterjee, Vice President, Titan

"Fed days tempt people to do something. Most of the time the better move is nothing. Portfolios that hold up when rates stay higher for longer are built that way in advance, not reshuffled the afternoon of a press conference."

|

|

|

Titan Global Capital Management, Inc.

PO Box 4668 | PMB 85274

New York, New York 10163-4668 US

© 2026 Titan, All rights reserved.

|

As of the time of publishing, Alphabet Inc. (GOOG), Meta Platforms, Inc. (META), Microsoft Corporation (MSFT), and NVIDIA Corporation (NVDA) are holdings in Titan's Flagship strategy.

Advisory services are provided by Titan Global Capital Management USA LLC ("Titan"), an SEC-registered investment adviser. Titan’s affiliate, Titan Global Technologies LLC (“TGT”), is an SEC-registered broker-dealer. Both Titan and TGT are subsidiaries of Titan Global Capital Management, Inc. This content is for informational purposes only and is not investment or financial advice, tax or legal advice, an offer, solicitation of an offer, or advice to buy or sell securities or other products offered by Titan, TGT, or any third party. Any mention of companies, securities, asset classes, or investment strategies does not constitute affiliation, an endorsement, or a recommendation.

References to investment themes are based on Titan’s internal research and opinion as of the date of this communication. Any descriptors used should not be construed as a promise of quality or a guarantee of performance. Statements made in these communications represent opinions and conjecture, and should not be construed as a guarantee of future results. This communication may contain forward-looking statements, which are subject to inherent risks and uncertainties that could cause actual results to differ materially. They should not be relied upon when making investment decisions. We do not undertake any obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events, or otherwise.

References to specific stock performances are provided for historical market context and are not indicative of future results or the performance of any Titan strategy. Any performance mentioned regarding individual securities reflects market performance for educational purposes only and is therefore shown gross of fees, where applicable. Actual performance may vary based on individual circumstances, including the specific timing of trade execution, which can impact the cost basis of any given investment. Valuation assessments in our communications are based on internal analysis and are for informational purposes only. They should not be the sole basis for investment decisions and may differ from others' views or assessments. No warranty is made regarding their accuracy or completeness. The mention of a security does not imply it is held in a Titan strategy. Where Titan does hold a company mentioned in our strategies, we’ll disclose it.

All investments involve risk, and the past performance of a security, particular strategy, or financial product does not guarantee future results or returns. Investment growth is not guaranteed. No strategy or asset guarantees the accumulation of wealth, and any potential benefits are subject to market, tax, and individual financial risks. Certain investments are not suitable for all investors. Diversification is a portfolio allocation strategy that seeks to minimize inherent risks by holding assets that are not entirely correlated. Keep in mind that while diversification may help spread risk, it does not ensure a profit or protect against loss. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. There is always the potential of losing money when you invest in securities or other financial products. Investors should consider their investment objectives and risks carefully before investing. The price of a given security may increase or decrease based on market conditions and clients may lose money, including their original investment and principal. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. Investment decisions should be based on individual financial circumstances, objectives, and risk tolerance. Investments in securities are not FDIC insured. Please visit www.titan.com/legal for additional disclosures.

|

|

|

|